Bank of America (BofA) is urging investors to use the recent US equity pullback as an opportunity to selectively build long exposure. As part of its research note, BofA has also named 10 stocks it believes are best positioned to outperform in Q2 2026 as macro and geopolitical headwinds begin to stabilise.

The call comes amid heightened volatility triggered by geopolitical escalation and policy uncertainty. For example, the S&P 500’s recent decline below 6,600, according to BofA strategists, has begun to ‘kick‑start policy panic’, although technical indicators have not yet reached levels typically associated with full capitulation.

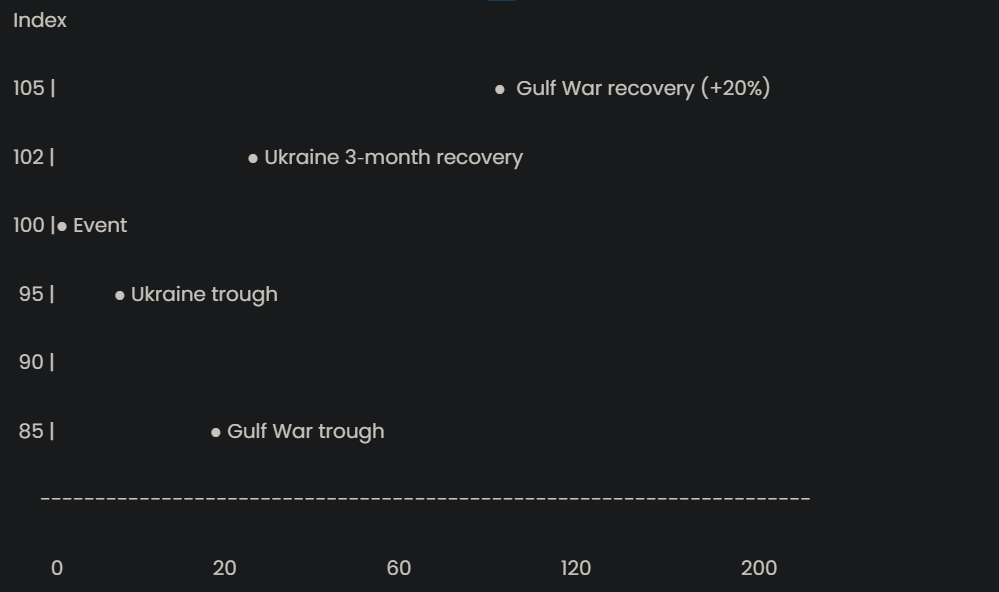

BofA notes that history continues to favour buying geopolitical drawdowns. Illustrating the point, BofA calculates that, on average, the S&P 500 has fallen approximately 10% during geopolitical shocks, before fully recovering within three months. However, the bank cautions against indiscriminate buying, recommending investors tilt toward large‑cap value, strong balance sheets, and idiosyncratic catalysts.

Within this framework, BofA has identified 10 US stocks rated Buy, spanning consumer, financials, industrials, technology, healthcare, media, defence, and real estate.

Past geopolitical shocks

Trading days since geopolitical shock

NB: Index level normalised to 100 at event date. Dots reflect documented historical milestones, not interpolated prices.

🔻 Phase 1 – Shock Absorption

‘Policy panic begins before fundamentals break.’

- Initial sell‑offs reflect uncertainty, not earnings collapse. Liquidity and positioning dominate price action

🔻 Phase 2 – Capitulation Window

‘Geopolitical drawdowns historically stop short of systemic stress.’

- Ukraine‑related sell-off peaked quickly

- Gulf War drawdown deeper due to recession + oil shock

- Both created forward return asymmetry

🔺 Phase 3 – Recovery & Re‑rating

‘Markets recover before headlines improve.’

- Gulf War: +20% gain between Desert Storm launch and victory parade

- Ukraine: positive 3‑month equity returns despite prolonged conflict

- Large‑cap, liquid equities lead rebounds

BofA’s top 10 stocks for Q2 bounce

1. Amer Sports (AS)

Investment Thesis: Earnings Upside Optionality

- Conservative guidance creates room for near-term beats

- Multi-year growth driven by retail expansion, product innovation, and geographic scaling

Growth Drivers:

Sales Growth Drivers

Retail Expansion ████████

Product Innovation ███████

Geographic Expansion ██████

2. Boot Barn (BOOT)

Investment Thesis: Overdone Pullback

- Stock down ~20% post-earnings → valuation reset

- Forecast: 14% revenue growth / 17% EPS growth (FY2027)

Store Expansion Pipeline:

Annual Store Growth Target

15% ┤ ███████████

12% ┤ █████████

0% ┴──────────

3. Citigroup (C)

Investment Thesis: Event-Driven Re-rating

- Key catalysts: Earnings (14 Apr), Investor Day (7 May)

- Expected return on tangible common equity target: 13%–15%

Catalyst Timeline:

14 April → 7 May

Earnings → Investor Day

4. ITT (ITT)

Investment Thesis: Multi-Sector Tailwinds

- Industrial demand recovery

- SPX Flow acquisition (largest in company history)

- Rising defense exposure

Revenue Mix Tailwinds:

Industrial Demand ████████

M&A Contribution ██████

Defence Exposure █████

5. MongoDB (MDB)

Investment Thesis: AI + Cloud Rebound Play

- Shares down ~28% → attractive entry point

- Strong demand for Atlas cloud platform

- Positioned for AI-driven workloads

Valuation Reset vs Opportunity:

Price Movement

Peak ┤ █████████████

Now ┤ ███████

Drop ┤ -28%

6. Meta Platforms (META)

Investment Thesis: Growth at Value Multiple

- Trading at 17x 2027E earnings vs 19x market

- AI catalyst: “Avocado” model launch

Relative Valuation:

Forward PE

S&P 500 ███████████████ 19x

META █████████████ 17x

7. RTX (RTX)

Investment Thesis: Defence Spending Upswing

- Beneficiary of missile & munitions replenishment

- Increased production frameworks (Tomahawk, AMRAAM, etc.)

Defence Demand Outlook:

Pre-Conflict Demand ██████

Post-Conflict Demand ███████████

8. Spotify (SPOT)

Investment Thesis: AI Fears Overstated

- Strong positioning in streaming ecosystem

- Investor Day (21 May) = re-rating catalyst

Narrative Shift:

Market Concern: AI Disruption ███████

BofA View: Overblown ███

Upside Potential █████████

9. Thermo Fisher Scientific (TMO)

Investment Thesis: Post-Weak Quarter Recovery

- Clario acquisition adds ~$1bn revenue (FY 2026)

- Margin recovery expected

Revenue Impact:

Base Revenue █████████████

Clario Addition ██ (+$1bn)

Total ███████████████

10. Welltower (WELL)

Investment Thesis: Operating Leverage Inflection

- Occupancy: 89.5% → nearing acceleration threshold

- Benefiting from peak leasing season

Occupancy vs Leverage:

85% ┤ ███████

88% ┤ █████████

90% ┤ ███████████ ← Inflection Zone

Strategic Takeaways

1. Buy the Dip—But Selectively

- Historical patterns favour recovery after geopolitical shocks

- Not yet full capitulation → staged entry approach preferred

2. Blend Value + Growth

- Value: Citigroup, RTX Corp.

- Growth at reasonable price: Meta Platforms, MongoDB

3. Focus on Catalysts

- Earnings events

- Investor days

- M&A integration

- AI product launches

You might also like: