Investors have been antsy about Adobe’s (ADBE) future for more than a year and now they are facing the added uncertainty of leadership change. Shantanu Narayen’s resignation announcement came out of the blue and knocked investors for six, sending the stock plunging overnight.

Pre-market data has the share price opening more than 8% lower later today, close to multi-year lows.

| Adobe (ADBE) | Price: $248.42 (-8) | Market cap: $119bn |

Narayen will remain in the role until a successor is named and stay on as board chair to support the transition. Even so, he’s been running the show since 2007, when the stock traded around the $40 mark, and been an ‘Adobe man’ for nearly 30 years. It’s a big deal and the timing is not great.

Adobe stock has fallen 25%+ this year and is roughly 65% down on all-time $688 highs in November 2021.

AI growth accelerating

AI disruption questions continue to swirl around Adobe and the wider software space. Investors remain nervous about the San Jose-based firm’s competitive positioning against AI-native creative tools, so accelerating AI growth came as a crucial lift.

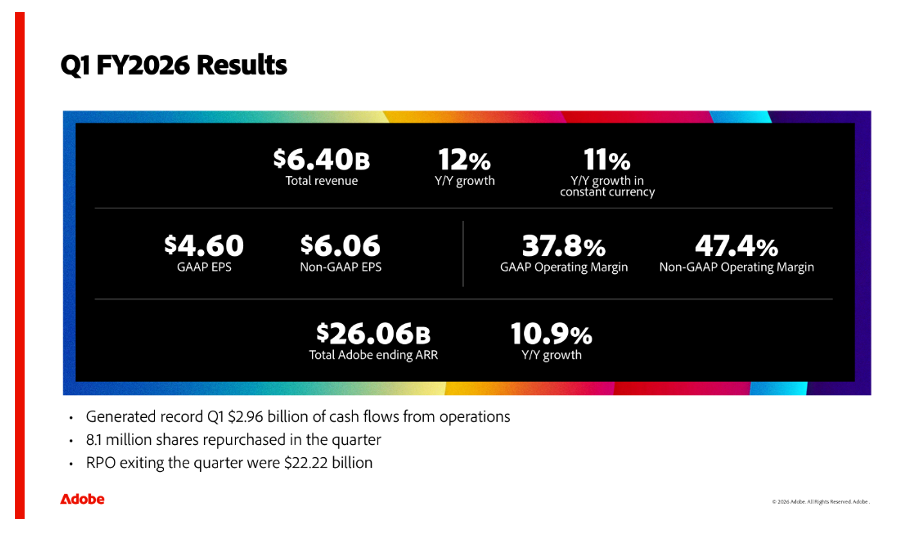

ARR, or annual recurring revenue, from AI-first products more than tripled year-on-year in Q1 2026 (to end February). ARR measures predictable revenue from existing contracts and subscriptions and tripling it in the AI segment is the proof point Adobe has been promising investors for several quarters.

In fact, Q1 was positive results-wise, with beats on earnings and revenue lines, and Q2 guidance lifted. Adobe posted adjusted EPS of $6.06 on revenue of $6.4 billion, well ahead of ‘Street’ consensus pitched at $5.87 EPS on $6.28 billion revenue.

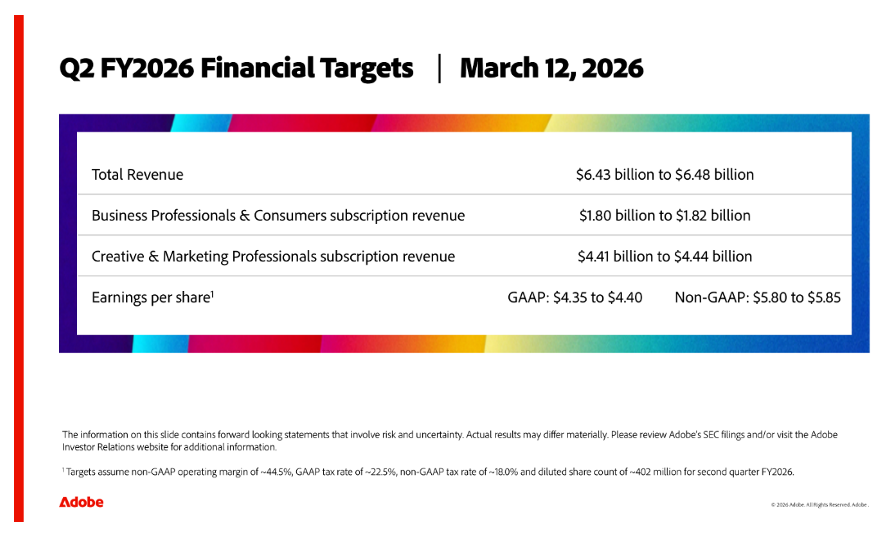

For Q2, Adobe is now guiding projected EPS $5.80-$5.85 on $6.43 billion-$6.48 billion revenue. That’s a 2%-3% increase on existing Wall Street estimates and implies 47% and ~10% year-on-year growth.

Questions over AI related opportunities and threats will likely hang over Adobe for the foreseeable future. AI is developing at such rapid pace that it is difficult to trust predictions for next year, never mind three to five out.

Even so, the valuation reflects this. This is a stock that has typically traded on a PE of 25+, yet is currently 11, on a 12-month rolling basis. An quality metrics like operating margins, returns on capital employed and equity have averaged 30%-40% over the past few years.

You might also like: