We believe shares in specialist manufacturer DiscoverIE (DSCV) are too cheap and deserve a higher rating.

The group makes customised electronic components for industrial uses, typically in mission-critical applications. Over the last decade, operating margins have more than tripled while shareholder returns have increased significantly.

However, this hasn’t been recognised by the market meaning the shares have derated substantially in recent years. Without stretching the valuation case, we can see the shares trading significantly higher in one or two years’ time.

| Share price: 620p | PE: 15.4x |

| Market Cap: £600m | Yield: 2.1% |

What does the company do?

Like many successful UK ‘compounders’, DiscoverIE manages a group of businesses in specialist niches providing customised technical solutions. Founded in 1986, today the group comprises 30 businesses in 20 countries in the UK, Europe, North America and Asia.

It supplies specialist electrical and electronic components to five distinct markets, each of which enjoys structural, sustainable growth: industrial and connectivity, medical, security, transport and renewable energy.

Each of these markets is part of a ‘mega-trend’, be it growth in automation and connectivity, the deployment of AI in the defence sector, wearable medical devices, the transport ‘revolution’ or decarbonisation.

Growing awareness of safety and security, as well as the need for predictive maintenance and efficient supply chains, are driving growth in the industrial use of fibre optics and wireless connectivity. Meanwhile, the use of electronic content in healthcare is rising due to growth in digital technologies and ‘smart’ medical devices.

Superior sales and earnings visibility

DiscoverIE’s customised products are made to customers’ unique specifications and are supplied over the life of the product design. Support is provided thereafter, even during challenges such as the pandemic which caused an upending of global supply chains.

Over 85% of sales come from long-standing relationships, with some customers having been loyal for over 30 years. With such a high degree of repeat business, visibility of future revenues is much better than for most industrial companies.

By increasing its embedded value and product range, the firm has grown organic sales by 7%/year over five years. This growth has been supplemented by earnings-enhancing acquisitions, which means margins have expanded at a faster clip than sales.

Financial performance 2020 to 2025

| 2020 | 2025 | Change | |

| Revenue (£m) | 303.3 | 422.9 | 39.5% |

| Operating Profit (£m) | 30.8 | 60.5 | 96.4% |

| Operating Margin (%) | 10.1 | 14.3 | 420bps |

| Pre-tax Profit (£m) | 26.5 | 50.1 | 89.1% |

| EPS (pence) | 24.4 | 38.7 | 58.6% |

| DPS (pence) | 3.0 | 12.5 | 317% |

Source: DiscoverIE

2025 revenue and operating profit by division

| Magnetics & controls sales | £261m | 62% |

| Sensing & connectivity sales | £162m | 38% |

| Magnetics & controls profit | £43m | 59% |

| Sensing & connectivity profit | £29.3m | 41% |

Source: DiscoverIE

Strong cash flow and balance sheet

Free cash flow for the year to 31 March 2025 increased by 9% to £40.4 million. The conversion rate of profit to cash was 106%, well above the group’s 85% target.

Disposal proceeds and deferred income from the 2022 sale of Acal BFi helped reduce net debt to £94.3 million. That took gearing to 1.3 times, below the 1.5 to 2 times target, providing scope for further earnings-enhancing acquisitions.

Over the last decade, the group has raised its targets for key strategic indicators nine times. Most recently, in June 2023, it set an operating margin target of 15% which it should meet in the near future.

The medium term margin target is 17%, with EPS growth seen above 10% and operating cash conversion still above 85%.

Recent trading has been robust

In H1 to September 2025, the group recorded a 3.5% increase in sales at constant exchange rates. Orders also rose 5%, and operating profit increased 5% to a record £30.2 million.

That lifted group operating margins to 14%, while free cash conversion was 104%, and the board confirmed FY earnings guidance. Trading momentum improved through the first half, with Q2 orders rising 8%, ahead of sales.

The firm said the sensing, connectivity and magnetics units saw good levels of organic growth. This came after a period of significant customer destocking in prior years.

The company also reported a strong pipeline of design wins and new opportunities. Meanwhile, the acquisition pipeline is still rich with opportunities to grow the business.

To limit the direct impact of tariffs, more production has shifted to North America. That has increased the proportion of locally made sales to US customers

At the same time, the firm is working to reduce the impact of tariffs on China-sourced imports by re-sourcing and/or passing on cost increases.

In the three months to December 2025, sales rose 5% while orders rose 9% with a book/bill ratio over 1:1. Both metrics mark an acceleration from H1, with the firm singling out the performance of the controls business.

The order book gives good coverage for the final quarter, gross margins stayed robust and cash generation stayed strong. As a result, the group is on track to deliver FY adjusted earnings in line with market expectations.

Consensus forecasts

| FY26E | FY27E | FY28E | |

| Revenue (£m) | 444.1 | 470 | 487 |

| Pre-tax profit (£m) | 53.1 | 58.5 | 63.4 |

| EPS (pence) | 40.2 | 44.0 | |

| DPS (pence) | 13.0 | 13.6 | 14.4 |

Source: DiscoverIE company-compiled consensus, data correct as of 12 December 2025

A compelling valuation

Turning to valuation, the shares currently trade at 620p or almost half their 2021 peak of £12.20. Adjusted EPS (earnings per share) are seen at 40p for the FY to March 2026 and 44p for FY27 against 22.4p in March 2021.

Therefore, the market is valuing the business on 15.4 times this year’s earnings and 14 times next year’s earnings. That compares with an astronomical 54 times during the pandemic, when margins and profits were considerably lower.

Despite the theory markets are efficient and share prices already discount all available information, investors can develop a blind spot. We believe that is currently the case with DiscoverIE. For a company with a 15-year record of 15% compound EPS growth, the current valuation looks far too low.

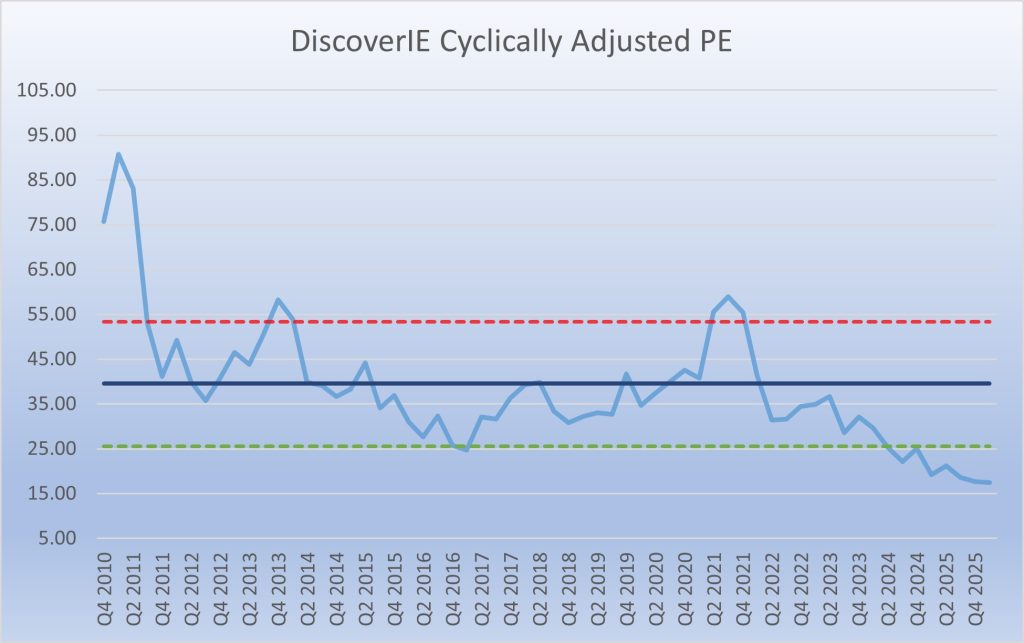

We think the shares can revert to 1 standard deviation below the mean or 25 times earnings (the green line on the chart) by March 2027. Assuming earnings are 44p as forecast, the implied price is £11 per share.

We don’t believe a base case of 1 standard deviation below the mean is outrageous, either – if anything it’s conservative. If the shares mean-revert fully (blue line) by March 2028, on 47.4p of EPS the implied price is £18.72.