Enterprise software firm Sage (SGE) reported a solid start to its 2026 financial year on Tuesday, posting double‑digit revenue growth in Q1. Importantly, it also signalled continued momentum in its transition toward cloud‑based services.

The upbeat trading update initially prompted a positive reaction in London, the shares jumping more than 5% in early dealings. But that optimism quickly subsided to leave the stock largely flat.

| Sage (SGE) | Price: £10.49 (+0.6%) | Market cap: £9.99bn |

The FTSE 100 accounting and business software provider said group revenue rose 10% year‑on‑year to £674 million for the three months ended 31 December, underpinned by broad‑based growth across all major regions. North America remained Sage’s largest and fastest‑growing market, delivering a 13% increase to £304 million. The UK and Ireland posted a 10% rise to £194 million, while revenue in Europe advanced 7% to £176 million.

Cloud busting growth

Cloud services continued to drive Sage’s overall performance, with Sage Business Cloud revenue rising 15% to £574 million. The company highlighted ‘balanced growth’ from both new customer wins and deeper adoption among existing clients. Cloud‑native products were a particular bright spot, expanding 24% to £253 million as more businesses shifted to fully online platforms.

Recurring revenue, an increasingly important metric for software companies transitioning to subscription models, also climbed 10% to £655 million. Sage said the result reflected sustained progress in ARR (annualised recurring revenue), which has been a key growth driver across recent periods. Software subscription revenue increased 12% to £568 million, lifting subscription penetration to 84%, compared with 83% a year earlier.

Analyst upbeat

Analysts welcomed the results. Charles Brennan at Jefferies noted that Sage’s 10% organic revenue growth represented a slight acceleration compared with the final quarter of fiscal 2025.

‘This revenue performance is strong in the context of the exit ARR growth in 4Q 2025 of 9.9%’, he wrote in a note to clients.

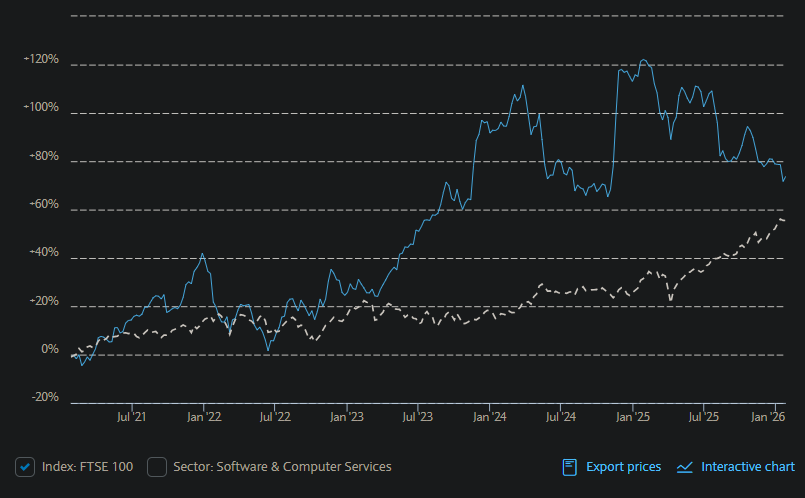

5 years of Sage share price returns

Source: Barclays, LSEG

Brennan added that while multi‑year contracts once again contributed a modest benefit of roughly 30 basis points, underlying momentum remained genuine. He said commentary during the company’s conference call, particularly regarding ARR trends, would be ‘key.’ But he argued the update carried a confident tone, especially around Sage’s efforts to ‘leverage the benefits of AI.’

Jefferies expects the business to continue delivering its typical pattern of roughly 2% sequential ARR growth into the second quarter. He added that the performance should support investor confidence in the sustainability of Sage’s growth trajectory.

Sage has for years been a steady grower with stable income support, making it a classic defensive growth play. Nothing today changes that.

Analysts predict EPS will grow more than 20% a year, on average, out to 2028 on revenue marginally below 10%. A dividend of 23.5p per share pencilled in for this year (to 30 September) impies a 2.2% yield.

You might also like: