According to the latest analysis by FactSet, last quarter S&P 500 companies posted the strongest earnings growth since Q4 2021. Not only that, the number of companies beating forecasts was the highest since Q2 2021.

Tech leads the way

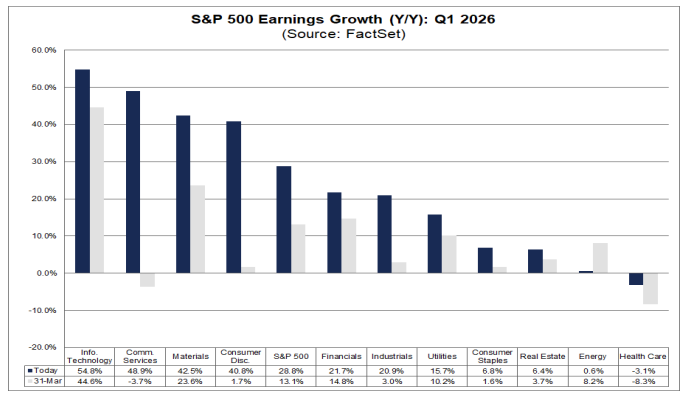

The average increase in earnings during Q1 2026 was 28.6%, the highest growth rate since the end of 2021. Unsurprisingly, the Information Technology sector showed the highest earnings growth at 55%.

Information Technology includes several Mag 7 stocks, such as Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT) and Nvidia (NASDAQ:NVDA). The second biggest increase in earnings came from the Communication Services sector, which includes Alphabet (NASDAQ:GOOG) and Meta Platforms (NASDAQ:META).

As we flagged in May, analysts raised their Q1 S&P 500 earnings growth forecasts sharply after the end of the quarter. Due to big ‘beats’ by Alphabet, Amazon (NASDAQ:AMZN) and Meta, the growth rate was hiked from 15% to 27%.

During Q1, 83% of S&P 500 companies posted earnings which beat forecasts, the highest level across the index since Q2 2021. At the same time, 59 companies posted positive EPS guidance for the quarter, also the most since Q2 2021.

What did companies say?

FastSet analysis shows the most common topics on conference calls were as follows:

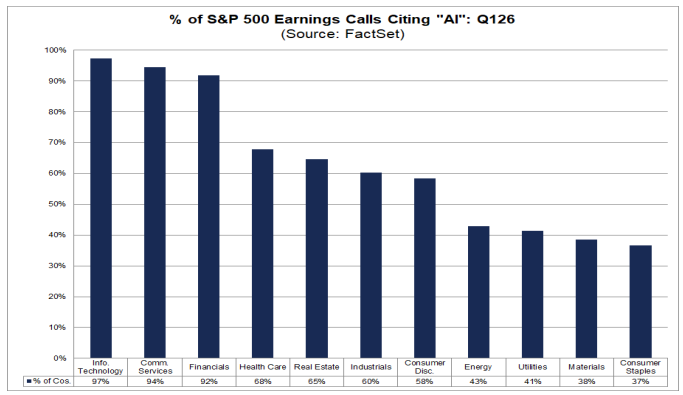

- 337 companies referenced AI at least once

- 220 companies referenced inflation at least once

- 218 companies referenced the Middle East at least once

- 149 companies referenced oil at least once

It’s probably no surprise the most common topic mentioned by companies on their Q1 conference calls was Artifical Intelligence (AI). In total 337 earnings calls or 68% of the total referenced AI, the highest level in 10 years.

Interestingly, companies which mentioned AI in their Q1 calls outperformed those that didn’t by quite a wide margin. Since 31 March, the average price increase for companies citing AI was 12.7% against 2.6% for companies which didn’t cite AI.

The second most common reference on conference calls was inflation, which increased in frequency for the third consecutive quarter to 220. This is well below the peak of 411 companies in Q2 2022, when US inflation peaked at 9.1%, but the trend is worth noting.

The Industrials sector had the highest number of mentions, but Consumer Staples and Materials saw the highest percentage of companies reference inflation. In contrast, mentions by Information Technology companies dropped while Communication Services saw no change.

What about the outlook for Q2?

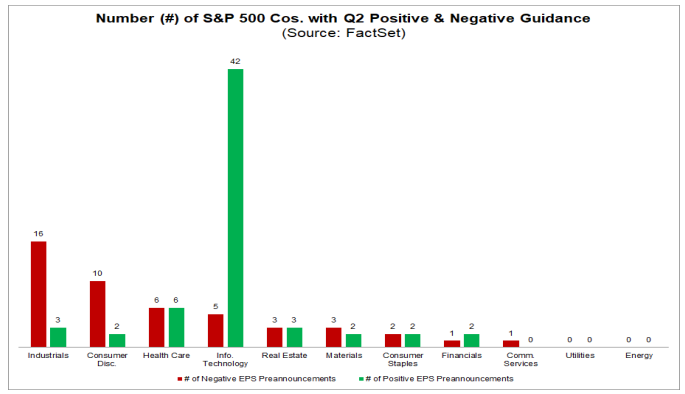

According to FactSet, analysts and companies are ‘more optimistic than normal’ in their earnings outlooks for Q2. As of the start of June, 109 companies had issued Q2 guidance with 62 positive outlooks and 47 negative outlooks.

The number of positive outlooks is well above the five-year average of 44 and the five-year average percentage (57% versus 41%). Due to these positive outlooks and analyst upgrades, Q2 EPS growth is expected to be 21.9% against 18.7% at the start of Q2.

Almost every sector is expected to report growth, with the biggest increases in Energy, Information Technology and Materials. The only sector expected to report a decline in earnings is Health Care.

If 21.9% is the actual growth rate for the quarter it will mark seven quarters of double-digit increases and the second quarter above 20%. For Q3 and Q4, analysts are forecasting growth rates of 25.3% and 22.8%, making the annual EPS growth rate 23.2%.