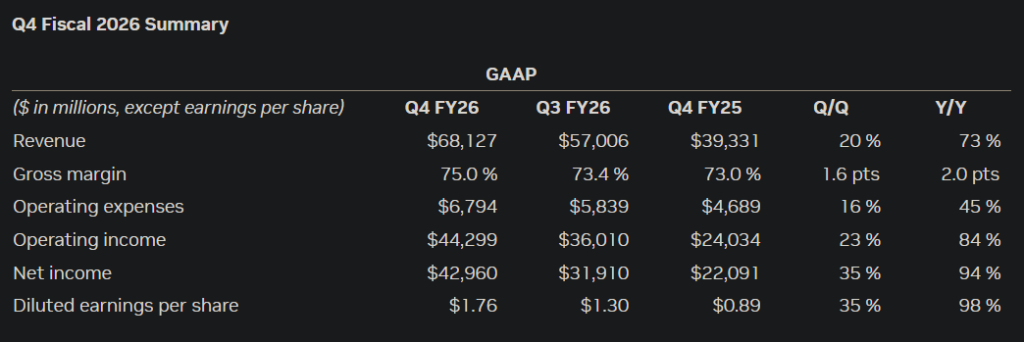

AI chip champ Nvidia (NVDA) smashed it again, outstripping Q4 2026 forecasts and upping guidance for Q1 2027. Yet the market’s muted response left analysts bemused and pondering if even standout execution may no longer be enough to excite investors deeply embedded in the AI boom.

For the second straight quarter, the chipmaker reported revenue that exceeded its own guidance (by roughly $3 billion this time), while its outlook was even more striking, implying about $5 billion above Wall Street expectations. Management also projected sequential growth for every quarter this year and signalled that strong momentum should continue well into 2027.

| Nvidia (NVDA) | Price: $198 (+1%) | Market cap: $4.75tn |

Markets unmoved

Investors could hardly ask for more, yet trading less than 3% below all-time highs and at a $4.75 billion market cap, the stock is promising rough 1% gains pre-market on Thursday.

‘We aren’t sure what else investors want to hear at this point’, remarked Bernstein’s Stacy Rasgon, capturing the growing sense of disbelief among Wall Street analysts.

Source: Nvidia

The soft market reaction may reflect how sky‑high expectations have become. Nvidia has now delivered sizable revenue beats for 14 consecutive quarters, setting a bar so high that even exceptional results risk appearing routine.

On the other hand, there’s a strong argument that on a rolling 12-month PE of 25, the stock is far from expensive given consistent 60%+ revenue and EPS growth. Analyst consensus was pitching 65% EPS growth this full year to end January 2027, and that was before the overnight beat.

Questions answered

Still, the latest numbers will help alleviate some short‑term concerns over the durability of AI‑driven spending. Sentiment toward AI‑linked equities has become more selective in recent weeks. Investors are increasingly focused on sustainability, returns, and differentiation within the broader tech sector.

Although demand for advanced AI chips remains robust, analysts warn that the benefits of the AI surge will not be evenly distributed across the industry. That may be true, but you’d hard pressed to find many that don’t see Nvidia capturing a huge chunk of AI growth in the years to come.

Nvdia Q4 webcast – https://events.q4inc.com/attendee/412427890

Morgan Stanley’s Joseph Moore described the results as ‘the largest, cleanest beat and raise in the history of the semis industry’, surpassing even Nvidia’s performance from the previous quarter. He noted that while the muted stock reaction was surprising, longer‑term debates, not near‑term fundamentals, appear to be weighing on the share price.

Raymond James analyst Simon Leopold expressed similar confusion, saying demand remains strong and execution continues to impress.

Primary economic growth engine

Stifel’s Ruben Roy reiterated his view that computing power has become the primary economic engine globally. Nvidia’s rapid product cycle, including the upcoming Vera Rubin platform, reinforces what he sees as a multi‑generation leadership position.

Source: Nvidia

Bank of America attributed the subdued stock response to ongoing market concerns about AI fatigue, mixed segment upside, and limited new commentary on Nvidia’s massive 2025–2026 data‑centre pipeline.

Even so, BofA’s Vivek Arya called the reaction ‘short‑term noise.’

Barclays analyst Tom O’Malley pointed to Nvidia’s recent $20 billion acquisition of Groq assets, IP and talent (focused on high-performance inference technology) as a potential catalyst heading into its March GTC (GPU Technology Conference) event, calling the company ‘the most interesting name in the group’.

Disclaimer: The author Steven Frazer has a personal interest in Nvidia.

You might also like: