AI chip champion Nvidia (NVDA) is set to report quarterly earnings after the bell on Wednesday, 25 February and expectations couldn’t be higher. After 13 consecutive quarters of beats and the stock +35% over the past year, there’s a lot riding on this quarter for a stock that almost every investor owns (one way or another). Nvidia Q4 earnings could set tone for global stock markets.

That said, the shares have flatlined this year, and haven’t done much since last summer, pulling the PE to levels seen only three times since 2020 (12-months rolling PE 24).

Growth momentum crucial

Last quarter delivered the goods. Nvidia posted $1.30 of EPS on $57 billion revenue, beating topline forecasts by more than $2 billion, and outstripping EPS estimates of $1.26 consensus.

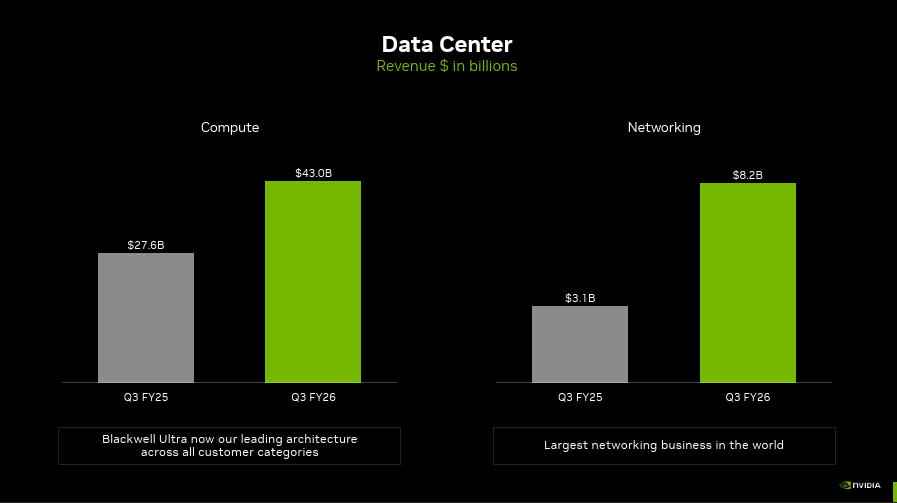

Data centre revenue hit $51.2 billion, up 66% year-on-year, with networking revenue more than doubling to $8.2 billion. Gross margins came in at 73.6% non-GAAP, ahead of guidance.

But the setup wasn’t perfect. Inventory jumped 32% sequentially to $19.8 billion, and China sales evaporated because of export restrictions. Jensen Huang acknowledged H20 chip sales were only around $50 million in Q3 after ‘sizable purchase orders did not materialize.’

Management assumed zero data centre compute revenue from China in Q4 guidance, which carries forward into this report.

Since then, shares have traded mostly sideways. The stock closed at $187.90 on 19 February, down 0.5% year-to-date.

Heavy analyst conviction

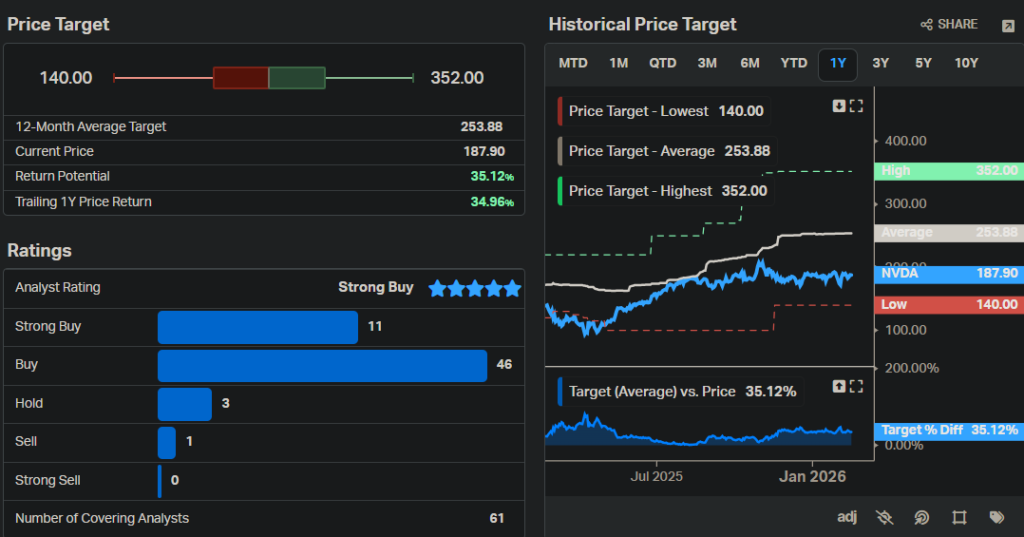

Yet Wall Street analysts remain verging on the euphoric, with 57 of the 61 that cover the stock recommending clients buy the stock. There is just one seller. Price targets also remain bullish, with a peak to low 12-month range of $352 to $140, leaving the average pitched at $254, implying 35% upside.

This optimism can be traced back to several things, not least a deluge of major strategic agreements, including a flagship partnership with Facebook-owner Meta Platforms (META), while all the major cloud hyperscalers have ramped AI capex guides far beyond Wall Street expectations.

Source: Koyfin

The $65.5 billion Q4 revenue guide implies 15% sequential growth from Q3’s $57 billion, and more than 70% year-on-year. That’s a meaningful step-up, especially with China revenue still zeroed out in guidance. Management guided gross margins to around 75%, which would mark continued improvement despite rising input costs.

Blackwell execution, Rubin vis

The key focus will be whether Blackwell chipset revenue justifies the hype. On the Q3 call, CEO Jensen Huang laid out $500 billion in combined Blackwell and Rubin visibility through the end of calendar 2026, with roughly $150 billion already shipped as of last quarter.

Huang described demand as ‘off the charts’ and said ‘the clouds are sold out’ with installed GPU capacity fully utilised across Blackwell, Hopper, and Ampere generations. Keep in mind, these quotes came ahead of most recent hyperscaler capex guides – Meta $115 billion-$135 billion, Alphabet $175 billion-$185 billion, Amazon $200 billion. All those numbers were all way ahead of Wall Street’s expectations.

Guidance will set tone

Gross margin expansion matters too, so it’s encouraging that CFO Colette Kress has said Nvidia is working to hold margins ‘in the mid-seventies’ for fiscal 2027 despite rising component costs. The path from 73.6% in Q3 to 75% in Q4 will show whether Nvidia can maintain pricing power as Blackwell scales.

Guidance for fiscal 2027 will clearly set the tone for Nvidia stock performance, but possibly also for wider AI, chips, tech… perhaps entire equity markets. Wall Street expects the company to guide to $1.66 EPS on $70.96 billion revenue in Q1 2027, implying 60%+ year-on-year topline growth and earnings more than doubling.

With a staggering $4.57 trillion market cap right now, well-received Q4 2026 earnings and bullish Q1 2027, guidance really could put $5 trillion in play over the coming months.

Disclaimer: The author Steven Frazer has a personal interest in Nvidia.

You might also like: