Yardeni Research argues that equities offer compelling value at current levels, citing a rare combination of meaningfully compressed valuation multiples and resilient earnings momentum. In the firm’s view, the recent market adjustment has improved forward return potential rather than undermined fundamentals.

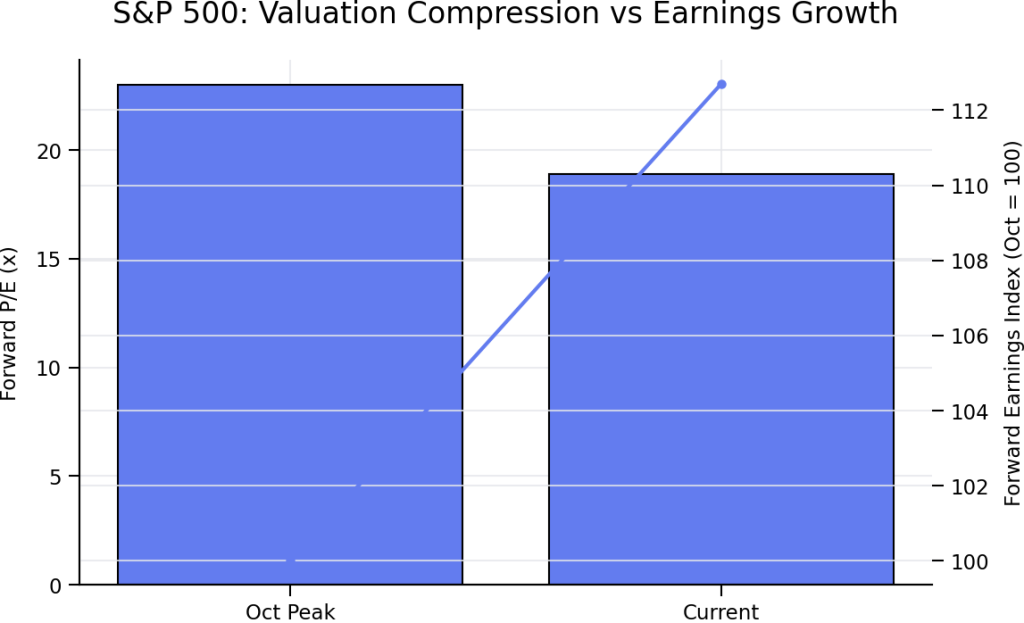

The firm notes that the S&P 500’s forward price‑to‑earnings (PE) ratio peaked near 23x in October and has since declined by 17.8% to 18.9x. Over the same period, forward earnings rose 12.7% to record levels, highlighting that the de‑rating has occurred alongside — rather than because of — weakening profit expectations.

Chart 1: Valuation Compression vs Earnings Growth

This chart highlights the disconnect between falling valuations and rising earnings, which is central to Yardeni’s bullish argument.

Investment take:

- The S&P 500’s forward PE has fallen from 23x to 18.9x (‑17.8%)

- Over the same period, forward earnings climbed ~12.7%, reaching record levels

- The multiple contraction has therefore come from sentiment and macro risk, not deteriorating fundamentals

- Historically, this setup has been associated with improving forward returns once uncertainty stabilises

Yardeni attributes the initial valuation contraction to concerns around AI‑related profitability, followed by a sharper multiple decline amid fears that escalating geopolitical tensions could trigger a global recession. However, the firm emphasises that earnings expectations have remained remarkably resilient throughout this period.

’Despite the typical pattern of estimates drifting lower as reporting season approaches, analysts’ Q1 forecasts held steady, even amid the war. More notably, consensus estimates for Q2 through Q4 have continued to move higher’, Yardeni observed.

Yardeni Research

Earnings momentum broadening

Beyond headline S&P 500 dynamics, Yardeni highlights a broadening earnings recovery across the market’s capitalization spectrum. Forward earnings expectations for the S&P 400 (mid‑caps) and S&P 600 (small‑caps) are also trending higher, reinforcing the case that profit growth is no longer narrowly concentrated.

At the sector level, Consumer Discretionary, Consumer Staples, Financials, Industrials, and Utilities have all reached record forward earnings, underscoring the depth of the earnings expansion.

Chart 2 — Forward Profit Margins Remain at Record Highs

This chart reinforces the durability of the earnings cycle and the quality of current profit growth.

Key observations:

- S&P 500 forward profit margin: ~15% (record high)

- Information Technology: ~31.4%, underpinning index‑level profitability

- Financials: ~21.4%, the second‑highest margin in the index despite a notable valuation de‑rating

Investment implication: Margin strength provides a buffer against macro shocks, supports cash generation, and weakens comparisons to prior valuation‑led bubbles.

Meanwhile, S&P 500 forward profit margins have risen to a record 15%, led by the Information Technology sector, where margins stand at 31.4%. Yardeni argues that these margin dynamics provide a durable cushion against macro volatility.

Technology valuations re‑align

Yardeni also points to a notable convergence in valuation between Technology and the broader index. The IT sector’s forward PE has declined to 20.7x, now roughly in line with the S&P 500’s 19.9x multiple.

‘For investors with a multi‑year horizon, this represents an attractive entry point’, the firm said, noting that the sector’s earnings quality, margin profile, and cash‑generation capacity remain materially stronger than in prior cycles.

Yardeni Research

The firm explicitly rejects comparisons to the dot‑com bubble. While Information Technology and Communication Services now account for 43.6% of total S&P 500 market capitalisation, exceeding late‑1990s concentration levels, Yardeni stresses that today’s earnings support is fundamentally different.

Those two sectors currently generate 42% of S&P 500 forward earnings, leaving only a 1.6 percentage‑point gap between earnings share and market‑cap weight. At the dot‑com peak, that gap exceeded 15 percentage points, reflecting valuation excess rather than profit dominance.

‘Today’s market concentration is well deserved’, Yardeni concluded.

Yardeni Research

Financials de‑rating overdone

Within the Financials sector, Yardeni identifies a potential valuation disconnect. The sector’s forward PE has fallen to 14.3x from 16.4x, despite maintaining the second‑highest forward profit margin in the S&P 500 at 21.4%.

The firm suggests this de‑rating may prove excessive if concerns around private‑credit stress remain contained, positioning Financials as a potential beneficiary of valuation mean reversion.

Finally, Yardeni notes that corporate insiders have recently turned more constructive, stepping up buying activity as equity prices weakened further. According to analyst Michael Brush, insiders have become increasingly bullish over the past two weeks — historically a supportive signal for forward market returns.

Bottom Line

In Yardeni Research’s assessment, the market’s recent correction has improved valuation support without breaking the earnings cycle. With profit growth broadening, margins at record highs, and insider behaviour turning supportive, the firm views current conditions as constructively bullish, particularly for investors willing to look beyond near‑term geopolitical noise.

You might also like: