Shares in data centres critical kit supplier Vertiv (VRT) have jumped 40% in a week, adding $27 billion to its market cap. The name may not be familiar to many UK investors but plenty will own it – it is a top 10 stake in both the Blue Whale Growth fund and Smithson Investment Trust (SSON).

| Vertiv (VRT) | Price: $248.51 (+24.49%) | Market cap: $95bn |

The stock had been heading higher into Q4 2025 earnings, but it was the publication of those results that really sent the stock into bonkers territory.

Faster growth, record orders

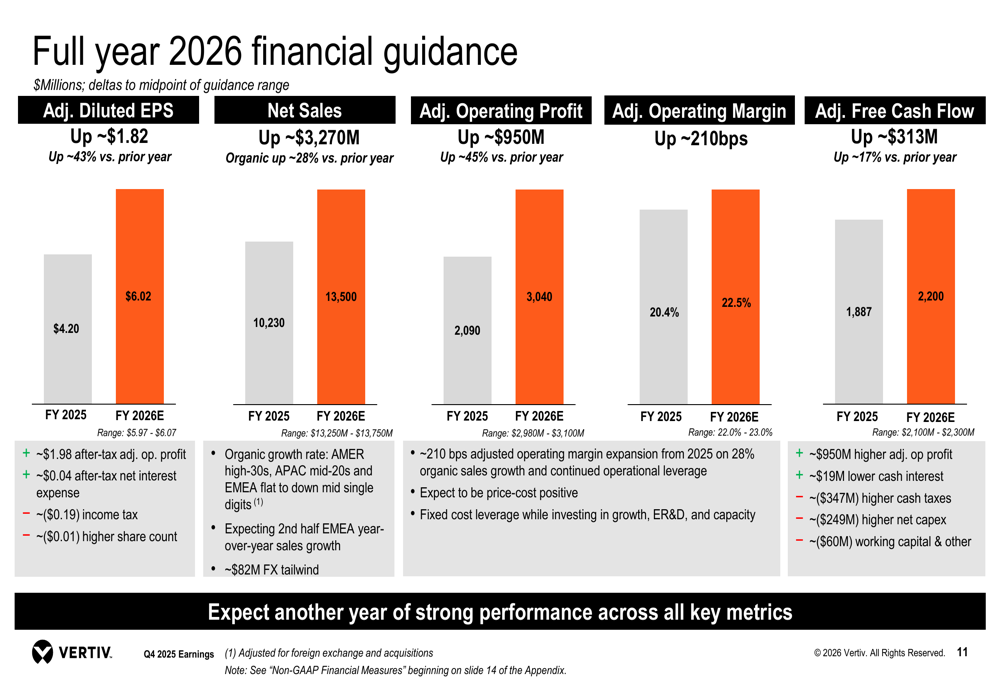

Vertiv expects full-year 2026 net sales of $13.25 billion-$13.75 billion, above the $12.39 billion consensus estimate. Adjusted diluted EPS is projected at $5.97 to $6.07, miles ahead of the $5.33 estimate. These figures demonstrate why Blue Whale Growth’s favourite Vertiv is experiencing such bonkers momentum right now.

The company also forecasts adjusted operating margins of 22% to 23%, far better than last year’s 20.4%, and free cash flow of $2.10 billion to $2.30 billion, supported by record backlog and continued AI-driven demand. For those asking why Blue Whale Growth favourite Vertiv is going bonkers, it is largely because of these robust forecasts and AI impact.

Orders were the standout metric. Organic orders rose 252% year-on-year, pushing the book-to-bill ratio to about 2.9x. Backlog reached a record $15 billion, more than double the level of a year earlier, providing strong revenue visibility.

AI infrastructure playbook

Vertiv continues to benefit from the global buildout of AI data centres. Hyperscale and colocation operators have been spending heavily on data centre infrastructure. Power systems, thermal management and high-density infrastructure required to support AI workloads means significantly upping demand for energy and cooling capacity than traditional cloud environments. With this backdrop, it’s obvious why Vertiv is going bonkers—with AI driving unprecedented demand.

That investment will be far larger in 2026, as we have seen in recent earnings from hyperscalers like Amazon (AMZN), Alphabet (GOOG) and Microsoft (MSFT) – great news for Vertiv.

A year of rampant growth

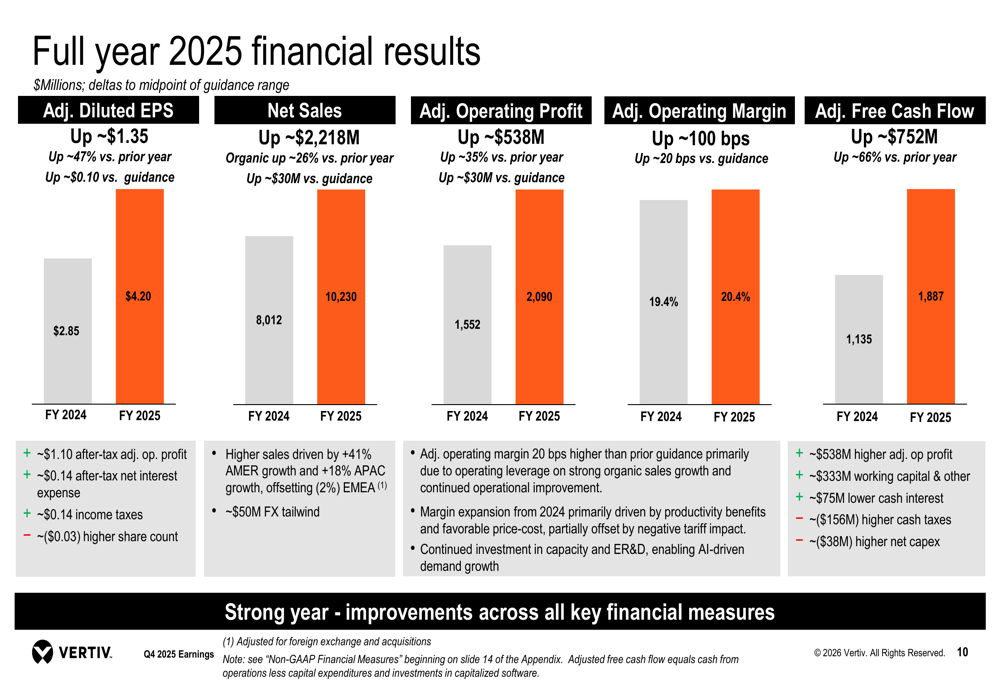

For full-year 2025, Vertiv delivered organic sales growth of 26%, while diluted EPS rose 166% and adjusted diluted EPS increased 47%. Operating cash flow totalled $2.11 billion and adjusted free cash flow reached $1.89 billion.

Q4 net sales of $2.88 billion were up 23% year-on-year, and just shy of the $2.89 billion consensus estimate, but profit easily beat estimates. Adjusted EPS came in at $1.36, up from $0.99 a year earlier and beating analyst estimates of $1.30. These results help explain why Vertiv, a favourite of Blue Whale Growth, is going bonkers.

Cash generation was also strong. Q4 operating cash flow reached $1.005 billion, while adjusted free cash flow jumped 151% year-on-year to $910 million. Net leverage remained low at roughly 0.5x, giving the company flexibility to invest in capacity and technology.

Vertiv is clearly on a roll, one with increasing momentum as the giants of AI and data centres unleash investment capex on an unprecedented scale. No wonder the stock has smashed industry and index benchmarks over 1, 3 and 5 years, as detailed below.

| 1-year perf | 3-year perf | 5-year perf | |

| Vertiv | 101.77% | 158.17% | 63.71% |

| Industry | 87.82% | 50.63% | 22.97% |

| Index | 15.34% | 20.46% | 12.44% |

Source: Morningstar

Disclaimer: The author Steven Frazer has a personal interest in Blue Whale Growth.

You might Also like: