Cisco Systems (CSCO) delivered one of its strongest ‘beat-and-raise’ quarters in years, and the market reaction reflected a major shift in investor perception: Cisco is no longer being valued purely as a slow-growth networking incumbent. Investors are increasingly treating it as an AI infrastructure supplier with expanding software exposure.

The key debate after earnings is no longer whether Cisco benefits from AI spending, but whether the current AI momentum is sustainable enough to drive multiple years of accelerating growth and margin durability.

What Sharesify said ahead of earnings

| Cisco Systems (CSCO) | Price: $119.28 (+17%) | Market cap: ~$470bn |

📊 Headline numbers

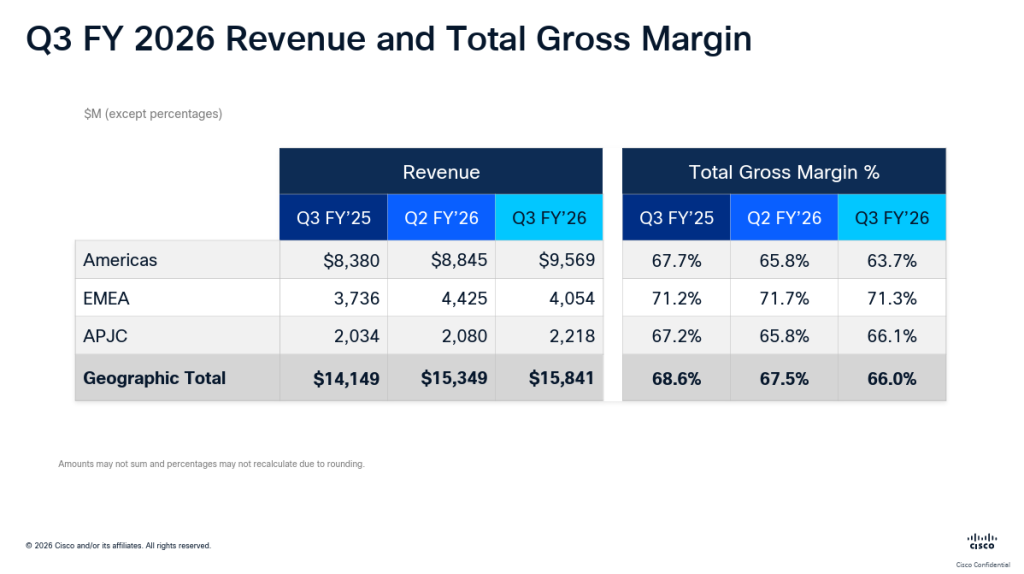

Cisco reported:

- Revenue of about $15.8B, up 12% YoY

- Non-GAAP EPS of $1.06

- Product revenue growth of 17%

- Networking revenue growth of 25%

- Total product orders up 35% YoY

- Networking orders up more than 50% YoY

Most importantly, management dramatically increased its AI expectations:

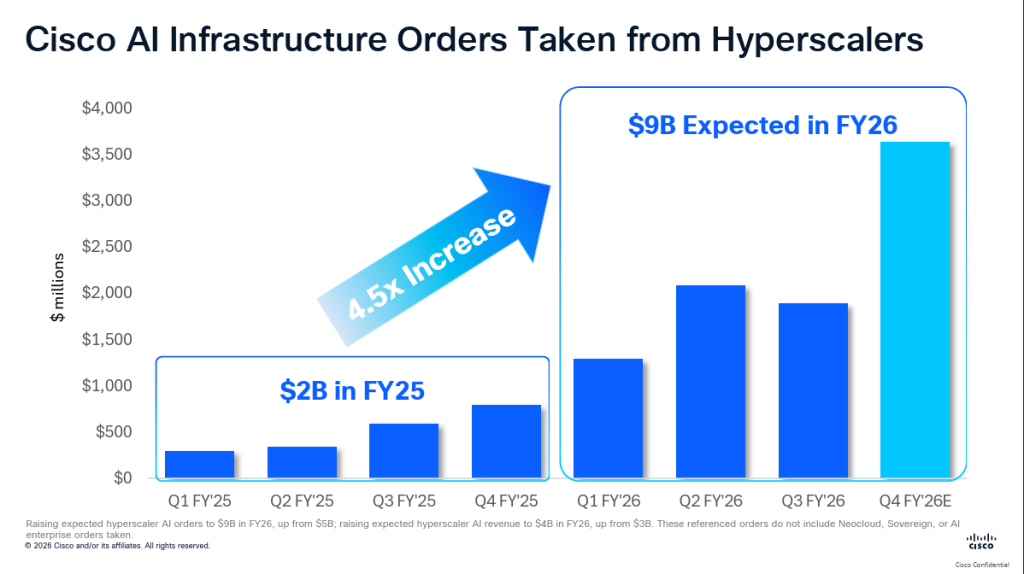

- FY2026 AI infrastructure orders guidance raised from $5B to $9B

- AI orders already reached $5.3B year-to-date

- Cisco now expects at least $6B hyperscaler AI revenue by FY2027

👉 That is the core reason the stock surged after earnings.

💡 AI opportunity: Cisco a ‘picks and shovels’ AI play

The biggest takeaway is that Cisco’s AI business has moved beyond pilot projects and into hyperscaler deployment scale.

Historically, Cisco struggled to participate in cloud capex cycles because hyperscalers often designed networking gear internally or bought white-box hardware. AI changes that dynamic because AI clusters require:

- ultra-fast networking,

- low-latency switching,

- optical interconnects,

- high-bandwidth Ethernet fabrics,

- and power-efficient silicon.

Cisco’s positioning improved substantially because of:

- its Silicon One architecture,

- partnership with Nvidia,

- ethernet-based AI networking,

- optics and switching integration,

- and Splunk-enhanced observability/security stack.

🧩 Management highlighted especially strong demand from hyperscalers and AI datacentre customers.

🧠 Why this matters strategically

For years, investors viewed Cisco as:

- mature,

- cyclical,

- low-growth,

- dependent on enterprise refresh cycles.

AI changes the narrative because hyperscaler spending cycles are:

- larger,

- faster growing,

- and structurally tied to multi-year AI infrastructure buildouts.

The most bullish signal was not just the $9B AI order target itself — it was the speed of the revision. Cisco moved from:

- ~$1B AI orders in FY2025,

- to >$5B expected in FY2026 earlier this year,

- to now $9B expected.

👉 That acceleration suggests Cisco may be taking share in Ethernet AI networking against proprietary alternatives.

🚀 The bull case

The bull thesis now looks like this:

- AI networking becomes a multi-year secular growth market.

- Cisco’s Silicon One gains hyperscaler adoption.

- Splunk drives higher software attach and recurring revenue.

- Enterprise networking stabilizes after several weak years.

- Security growth reaccelerates.

If that happens, Cisco could transition from:

- low-single-digit revenue growth

to - sustained high-single-digit growth with operating leverage.

That would justify a structurally higher valuation multiple than the stock historically commanded.

🌍 Growth guidance: the most important part of the quarter

The earnings beat mattered less than the guidance raise.

Cisco increased FY2026 revenue guidance to:

- $62.8B–$63.0B

from - $61.2B–$61.7B previously.

Q4 guidance also came in well above expectations:

- Revenue: $16.7B–$16.9B

- Non-GAAP EPS: $1.16–$1.18

That matters because investors were worried Cisco’s AI demand might remain mostly backlog/orders rather than convert into actual revenue.

This quarter showed conversion is happening.

What retail investors should watch next

Three metrics matter most going forward:

1. AI order conversion

Orders are impressive, but investors need to see:

- shipments,

- revenue recognition,

- and repeat customer spending.

If AI orders remain strong but revenue conversion slows, enthusiasm could fade quickly.

2. Enterprise demand stabilisation

Cisco still has significant exposure to:

- campus networking,

- enterprise switching,

- telecom,

- and traditional infrastructure.

AI alone cannot carry the whole company forever. Investors should monitor whether non-AI businesses stabilize.

3. Security and Splunk integration

Splunk remains critical to Cisco’s long-term transformation into a software/security platform.

If Splunk accelerates recurring revenue and improves cross-selling, Cisco’s valuation multiple could expand materially over time.

🧩 Gross margins: strong, but the pressure is real

Gross margin is becoming one of the most important issues in the Cisco story.

Cisco guided Q4 non-GAAP gross margin to:

- 65.5%–66.5%

That remains healthy by hardware standards, but it is below the ultra-high margins investors historically associated with Cisco.

Why margins are under pressure

Several factors are squeezing margins:

- rising memory costs,

- expensive AI components,

- optics and silicon costs,

- hyperscaler pricing pressure,

- and mix shift toward AI hardware.

Earlier in FY2026, Cisco already disappointed investors with lower-than-expected gross margins due to AI-related memory inflation.

🔁 This creates an important tension:

AI is boosting growth — but may dilute margins

AI infrastructure is:

- higher volume,

- faster growing,

- but potentially lower margin than legacy enterprise networking.

That means Cisco may evolve into:

- a faster-growing company,

- but not necessarily a dramatically more profitable one on a gross-margin basis.

Why margins still look better than feared

The encouraging part is that margins held up better than many investors expected despite the AI ramp.

👉 Management emphasised:

- Silicon One integration,

- owned intellectual property,

- and pricing actions.

That suggests Cisco still retains pricing power and operational leverage.

👉 For long-term investors, the key question is:

Can Cisco sustain mid-60s percent gross margins while scaling AI revenue aggressively?

If yes, earnings growth could remain very strong.

👉 Retail investor takeaway

This quarter likely marks a turning point for Cisco’s market narrative.

The company is proving:

- AI demand is real,

- hyperscaler traction is accelerating,

- revenue conversion is improving,

- and growth guidance is moving materially higher.

The biggest positive surprise was the jump from a $5B to $9B AI order outlook. That suggests management sees demand accelerating faster than Wall Street anticipated.

However, investors should avoid assuming this becomes a pure high-margin AI software story overnight.

🚫 Risks remain:

- hyperscaler spending cyclicality,

- margin compression,

- competitive AI networking pressure,

- and dependence on continued AI capex growth.

Still, compared with Cisco’s historical profile as a slow-growth networking vendor, this was arguably one of the strongest strategic quarters the company has delivered in years.

You might also like: