")

AIM-listed insurance and workplace benefits business Personal Group (PGH) is an exciting growth story with rising margins and a strong balance sheet. After a year of significant strategic progress in 2025, the business has entered 2026 with strong momentum.

Personal Group aims to be the champion of affordable and accessible insurance and benefits, keeping companies and their workforces happy, healthy and protected.

Insurance revenue and new premium sales are both growing at double-digit rates and 90% of revenue is recurring. With zero debt and £29 million of net cash, close to 30% of its market value, the company looks seriously undervalued.

| Price: 340p | Current P/E: 13.5x |

| Market cap: £106 million | Current yield: 7.5% |

What does the company do?

The group’s insurance provides employees with access to affordable individual policies for hospital, recovery and death benefit plans. Meanwhile, its award-winning Hapi platform offers extensive employee benefits, discounts and rewards. As well as being sold direct to employers, Hapi supports Sage’s (SGE) Employee Benefits offerings for small and medium-sized businesses.

The group’s range of offerings, platform and individual sales model with one-to-one employee engagement provides a strong proposition. Demand for its services, especially from workers with otherwise limited benefits and protections, is driving growth.

In 2025, management delivered on every customer metric, from acquisition to penetration and retention, generating impressive growth. CEO Paula Constant described it as ‘a brilliant year of progress’, with double-digit growth, EBITDA ahead of expectations and continued high retention levels.

We believe the group will perform even better through 2026 and beyond as it continues to innovate and expand. If we assume the rating reverts to its historic mean by the end of 2027, we could see the share price north of 600p.

A significant growth opportunity

For the financial year to December 2025, the firm increased revenue by 11% to a record £48.4 million. Over 90% of reported revenue came from recurring contracts in the insurance segment and benefit subscriptions.

Adjusted EBITDA increased 22% to £12.1 million, ahead of market expectations of £11.6 million. Pre-tax profit rose 23% to £8.4 million, while basic EPS rose 32% from 17.7p to 23.3p.

The group generated £9.9 million of cash from operations and ended the year with £29 million of cash and zero debt. The total dividend for FY25 was 23.3p, in line with earnings as per the group’s new policy, meaning a 41% increase.

Annualised new insurance sales increased 11% to a record £15.4 million and annualised premium income rose 12% to £40.5 million. Customer retention remained strong at 81.7%, while the firm made significant new client wins adding over 50,000 new potential customers.

The benefits platform generated annual recurring revenue of £7.3 million, up 9%, driven by continued uptake and new client wins. The group also extended and expanded its partnership with Sage, taking it into the Irish market for the first time.

With companies struggling to attract and retain good people, and high levels of workforce illness, the group’s offering is more relevant than ever. Having started 2026 with positive momentum, the firm has plenty of growth runway ahead of it and an expanding market to go for.

Below we show the company’s performance over the last decade, but in this case several caveats are needed. The 2016 results include £25 million of revenue*, £2.3 million of EBITDA* and additional earnings* from Let’s Connect, which was sold in 2024.

Furthermore, the company has invested significantly in Hapi and internal technology in recent years. This has generated higher revenue, but also increased depreciation and amortisation which has impacted reported EPS*.

Personal Group financial performance 2016-2025

| 2016 | 2025 | Change | |

| Revenue (£m)* | 53.6 | 48.4 | -9.7% |

| Adjusted EBITDA (£m)* | 11.4 | 12.1 | 6.1% |

| EBITDA margin (%)* | 21.3 | 25 | +370bps |

| Cash from operations (£m) | 6.4 | 9.9 | 54.7% |

| EPS (p)* | 29.7 | 23.3 | -21.5% |

| DPS (p) | 29.0 | 23.3 | –19.7% |

| Net cash/debt (£m) | 13.2 | 29.0 | 120% |

Source: Personal Group, data correct as of 24 March 2026

Long-term ambition to double sales and profits

The group has made major strides both in its insurance and benefits business over the last couple of years. In insurance, customer penetration has risen, particularly with its top 100 customers, and it has partnered with a benefits competitor to offer its insurance products.

In benefits, recurring revenue from Hapi has increased along with monetisation of the platform and it has won new clients. Also, its Innecto pay and reward consultancy business has rediscovered its mojo and is winning new clients.

Last year, CEO Paula Constant set out some bold targets for the firm and they were reiterated last month. The aim is to hit £100 million of sales and £30 million of EBITDA by 2030, including over £20 million in SaaS (software as a service) revenue.

To do that, first the group is targeting 300,000 new employee customers for its insurance business. Together with a high recurring base, that should take annual premium income to over £70 million or double the current figure.

Under the plan, 10% of group EBITDA will come from new insurance products and channels. On the benefits side, the group aims to double its client base and add another 10 partnerships to create 8,000 annual leads.

Current FY26 and FY27 forecasts

| FY26E | FY27E | |

| Revenue (£m) | 53.2 | 60.5 |

| Adjusted EBITDA (£m) | 14.0 | 16.2 |

| EBITDA margin (%) | 26.3 | 26.8% |

| EPS (p) | 25.2 | 30.6 |

| DPS (p) | 25.2 | 30.6 |

Source: Capital Access, data correct as of 24 March 2026

An attractive valuation

Turning to valuation, the shares currently trade at 340p which is around half their level of 10 years ago. For comparison, earnings per share in 2016 were 29.7p against 23.3p last year and a consensus of 25.2p this year.

In other words, the shares trade on a forward PE of 13.5 times today against 21 times a decade ago. Considering roughly 30% of the market value is in cash, the actual operating business is valued at well under 10 times earnings.

Granted, earnings haven’t grown that fast on an historic basis – we have assumed a CAGR of around 4% since 2001. However, that’s probably too conservative going forward as the currrent consensus puts FY27 earnings some 18% above our ‘trend’.

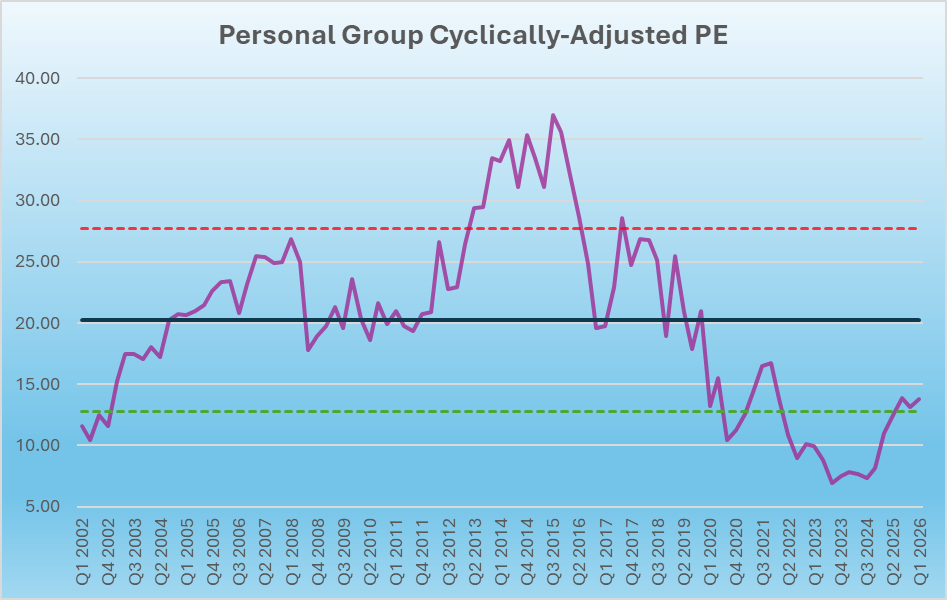

Yet, even using a low growth rate, on a cyclically adjusted PE basis the shares are cheap relative to their history. Scrolling back to 2024, they were trading more than one standard deviation below their 20-year mean.

We are big believers in the power of mean reversion when it comes to valuation – both to the upside and the downside. If the shares returned to their mean (the black line) by the end of 2027, based on the current 30.6p EPS forecast they would be worth over 600p. Even if they only reverted half-way to the mean, they would still be worth more than 450p against 340p today.

We should also flag that in addition to the share price upside, the stock offers a very attractive dividend yield. Compounding at 7.5% out to the end of 2027 adds another 15.5% to the total return.