When a company is due to report earnings, investors will look first at analysts’ forecasts, but they will also want to know the ‘whisper number’. This is the unofficial or ‘unspoken’ estimate, and is usually higher than the official consensus.

When investors anchor their expectations on the ‘whisper number’ rather than the consensus, which is typical in bull markets, it can cause problems. This is because they are setting a higher bar than is strictly necessary, raising the risk of a downside surprise.

Technology-driven Q1 ‘beat’

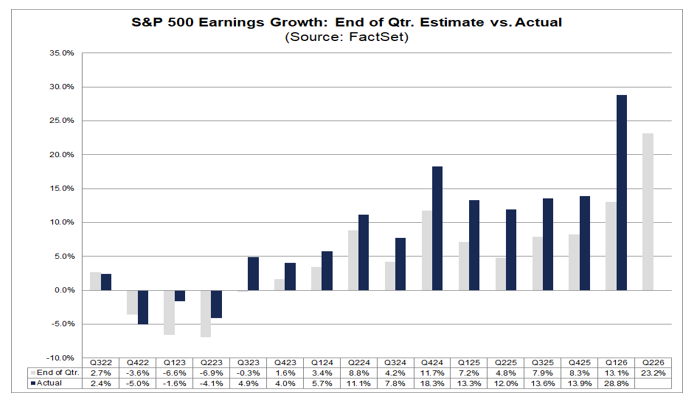

As we revealed in a previous article (below), analysts had originally forecast Q1 2026 US EPS (earnings per share) growth of 15%. After the end of the quarter, however, they revised their forecast sharply higher to 27% growth.

This was thanks to big ‘beats’ by technology firms Alphabet (NASDAQ:GOOG), Amazon (NASDAQ:AMZN) and Meta Platforms (NASDAQ:META). In the event, Q1 earnings rose by an average of 28.6%, beating even the 27% ‘whisper number’.

So what is the outlook for the Q2 earnings season, which kicks off this week with results from JPMorgan Chase (NYSE:JPM)? Today’s forecast, according to FactSet specialist John Butters, is for earnings to rise by 23.6%, marking a second quarter of 20%-plus growth.

Will Q2 earnings beat forecasts?

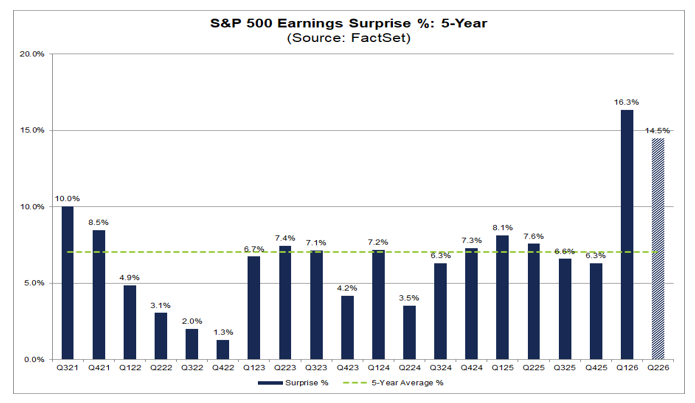

According to Butters, the actual US earnings growth rate has exceeded the quarter-end estimate in 37 of the past 40 quarters. That means it is highly likely earnings will surpass the end-June forecast, most likely due to more big ‘beats’ by technology comapnies.

Over the past 10 years, actual earnings reported by S&P 500 companies have exceeded estimates by an average of 7.4%. Over that period, on average 76% or three quarters of companies have reported actual EPS above the mean estimate.

As a result, from the end of the quarter through to the end of the earnings season, growth has risen by an average 6.2%. If we apply the same increase to the official end-June estimate of 23.2%, we get a ‘whisper number’ of 29.4%.

If we use shorter-term averages, that number rises further. Adding the average five-year ‘beat’, implied Q2 EPS growth becomes 29.6% while using the average of the last four quarters implied growth rises to 31.7%.

Implied Q2 EPS growth rates

| 1 year | 5 years | 10 years | |

| Average ‘beat’ | 9.2% | 6.4% | 6.2% |

| Implied Q2 growth rate | 31.7% | 29.6% | 29.4% |

Source: S&P500, FactSet

What are the risks?

The risks, as we said earlier, are the higher the ‘whisper number’ the greater the scope for disappointment. If investors anchor themselves on EPS growth of around 30% instead of sub-25%, we believe they are setting themselves up for a fall.

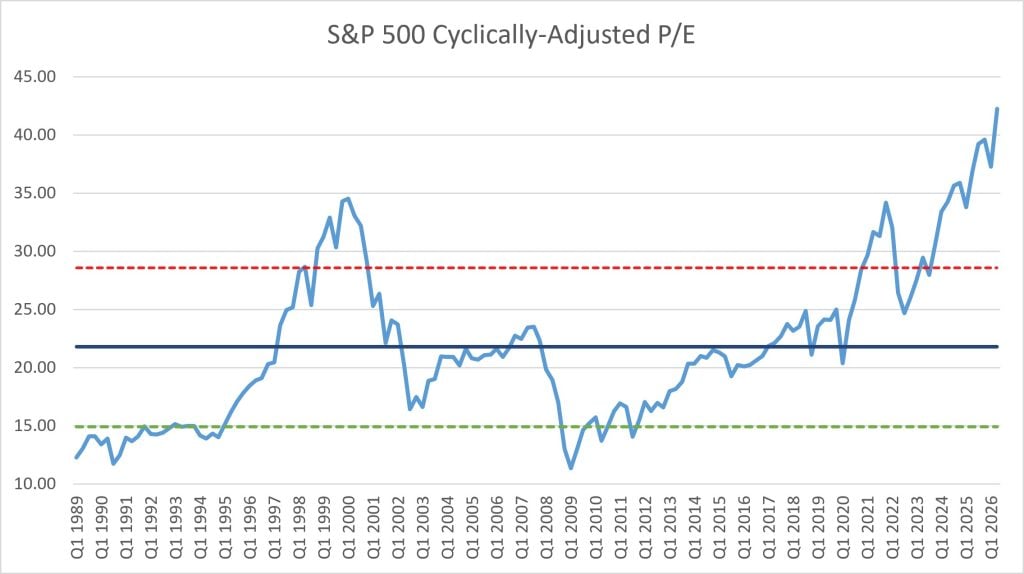

Normally, this might not matter overly, but it is widely accepted the US market is overvalued on several measures. Our preferred way of valuing stocks and markets is to see what we have paid for cyclically-adjusted earnings over several decades.

By smoothing out the peaks and troughs, we avoid situations where stocks trade on cycle-high or cycle-low earnings, which tell us nothing. We also end up with a mean valuation which we think of as ‘fair value’ based on through-the-cycle earnings growth.

As the chart below shows, on cyclically-adjusted earnings, the US market is trading at its most expensive level of the last 35-plus years. Therefore, if US earnings growth fails to meet the ‘whisper number’, either this quarter or at some point in the future, the downside could be considerable.

Note: solid blue line = mean; red dotted line = +1 SD (standard deviation); green dotted line = -1 SD