With the Strait of Hormuz still more or less shut to traffic, oil and gas prices remain at elevated levels. Brent crude oil futures continue to trade around $90 per barrel compared with $60 at the start of the year.

As Ecofin Redwheel fund manager Michel Sznajer describes it, Hormuz could be ‘the new Fukushima’. ‘Explosive price volatility, fuel rationing and demand-based restrictions evoke the systemic vulnerability felt after Fukushima’, says Sznajer.

Even if the Strait reopened tomorrow, it would take a long time for normal service to resume. Moreover, energy prices will still carry a ‘Hormuz premium’ according to Bloomberg Intelligence’s senior oil and gas analyst Salih Yilmaz.

That scenario has reignited the debate around energy security, alongside the need for energy efficiency. Unlike Fukushima, however, this time the world is ready to pivot at scale away from fossil fuels towards electrification more broadly, renewables, and more secure, local power systems.

The opportunity for renewables

According to the IEA (International Energy Agency), in 2025 around 60% of the world’s electricity was generated using fossil fuels. Some 80% of the world’s population lives in countries which are net importers of fossil fuels.

Yet, in the next five years, 65% of global electricity supply could come from renewable energy sources says the IEA. Over 90% of new renewable projects are cheaper than fossil fuel alternatives: wind and solar are 41% and 53% cheaper.

There are other arguments for renewable energy, such as population health and job creation. The WHO (World Health Organisation) estimates air pollution costs $8 trillion of economic health damage each year, equivalent to 6% of global GDP.

In addition, the clean energy sector creates more jobs than fossil fuels and already employs around 35 million people worldwide. For every dollar invested, renewable energy creates three times as many jobs as the fossil fuel industry.

Back in favour

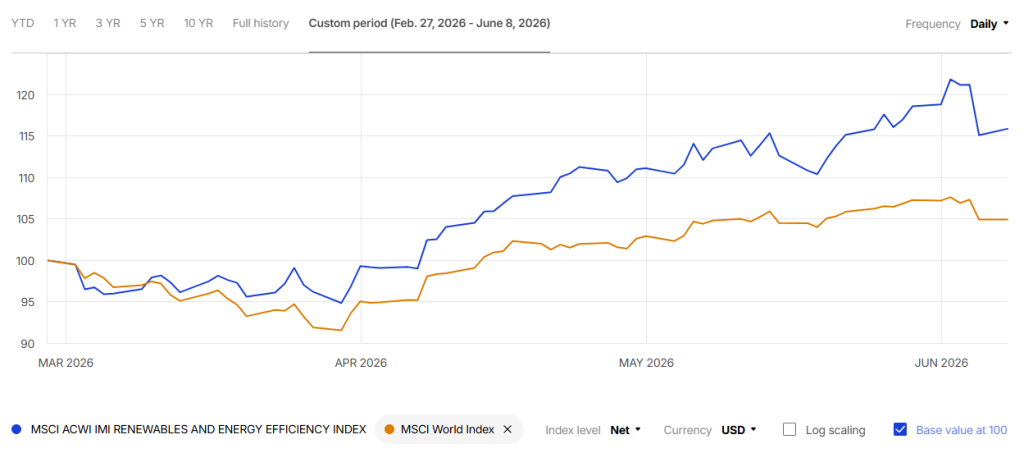

Since the start of the Iran conflict and the closure of the Strait of Hormuz, renewable stocks have been outperforming. From 28 February to date, the MSCI ACWI Renewables & Energy Efficiency Index has gained 16% while the MSCI ACWI World Index has gained 5%.

Source: MSCI

In fact, the ACWI Renewables & Energy Efficiency Index has comfortably beaten the All-World Index over the last year. That suggests renewable stocks have found favour again with investors after a period of several years in the wilderness.

That’s not to say there haven’t been some casualties along the way. For example, SDCL Energy Efficiency Trust (LON:SEIT) is working through a managed wind-down after shareholders rejected its proposed strategic overhaul.

Impax Environmental Markets (LON:IEM) is a shadow of its former self after carrying out a tender offer in May under pressure from activist investor Saba Capital. After 80% of shares were tendered, the much-reduced fund faces an extraordinary meeting where Saba could replace the entire board.

Last month, however, US Solar Fund (LON:USF) was the best-performing investment trust, rising 33% after revealing bid talks. Meanwhile, Bluefield Solar Income Fund (LON:BSIF) found itself the subject of a bid from electricity giant Drax (LON:DRX).

The bid for Bluefield Solar Income came at a 31% premium to the share price and just a 9% discount to NAV. That surprised analysts, who had predicted a take-out by private equity at a 20% discount to NAV at best.

Stick with the experts

While there are plenty of renewable energy stocks to choose from, even the experts can struggle to pick individual winners. Not only that, renewable stocks have on occasion blown themselves up, in some cases quite literally.

Last month, AIM-listed Clean Power Hydrogen (LON:CPH2) revealed one of its electrolysers suffered ‘significant’ damage during shutdown due to an unexpected error. On closer inspection, the damage was found to be so extensive the equipment was irrepairable, meaning further testing was impossible.

The firm said the unit required ‘substantial redesign’ to ensure the mixed gas system could be operated safely in all conditions. Sadly, it doesn’t have the financial, engineering or technical resources needed, so it has ceased operations and is evaluating its options.

Far better in our view to go with a fund or trust, where the manager takes responsibility for picking the portfolio. Again, there is no shortage of choice, but we like the following three funds for their combination of upside potential and income.

Foresight Environmental Infrastructure (LON:FGEN)

| Share price: 81.5p | Total Asets: £823 million |

| Discount to NAV: -22% | Dividend Yield: 9.8% |

Source: The AIC

Investors seeking a high-yield play on the climate change mitigation theme should consider Foresight Environmental Infrastructure (LON:FGEN). Currently trading at a wide 22% NAV discount, this quarterly dividend payer is the AIC Renewable Energy Infrastructure sector’s best five-year share price total return performer.

Known for its resilience, FGEN is more or less a ‘one-stop-shop’ for environmental infrastructure exposure. The bedrock of the portfolio is characterised by stable, predictable cash flows, inflation linkage, often supported by government subsidies or other regulatory mechanisms given the critical role its projects play in the decarbonisation drive.

Winterflood analyst Ashley Thomas believes the £823 million trust is well-positioned for organic NAV growth. Focused on the UK and mainland Europe, the portfolio is diversified across wind and solar assets, as well as anaerobic digestion, biomass, energy-from-waste and hydropower.

FGEN delivered resilient NAV growth in the quarter to March 2026, with NAV per share of 105.2p representing a 0.6p increase over the quarter. Updated power price forecasts driven by the escalation of the Middle East conflict lent some support.

Power generation was 2.6% ahead of budget in the quarter, with a strong performance from FGEN’s anaerobic digestion portfolio. Whilst wind, solar and biomass underperformed, performance across these sectors in March proved excellent.

The trust has set a target dividend for the year to March 2027 of 8.04p, which will be its 12th consecutive dividend increase since IPO.

Greencoat UK Wind (LON:UKW)

| Share price: 103.5p | Total assets: £4 billion |

| Discount to NAV: -22.8% | Dividend yield: 10.3% |

Source: The AIC

Conflict in the Middle East has served to remind politicians and investors of the economic importance of energy security. One trust playing its part in the quest to deliver clean power is Greencoat UK Wind (LON:UKW), whose fortunes are steered by specialist renewable energy investor Schroders Greencoat.

The FTSE 250 fund generates robust cash flows from investments in UK operating wind farms. Sharesify believes a 23% share price discount to NAV presents value- and income-seeking investors with a buying opportunity.

In April, Greencoat UK Wind warned the UK government’s change to the inflation link in renewable subsidies could reduce its net asset value (NAV) by between 3p and 5p per share. Shares in the first renewable investment trust to list on the London Stock Exchange’s main market wafted lower on the news.

Greencoat UK Wind closed 2025 with NAV per share of 133.5p, down from 151.2p as of December 2024, so a 5p reduction would lower that NAV by 3.8%. However, power price forecasting is a very complicated business with multiple moving parts feeding through to long-term assumptions.

The removal of carbon price support was expected over the longer term anyway. And Greencoat UK Wind won’t be the only fund to feel the impact of its removal on power price forecasts.

The resilience of the underlying portfolio is reflected in the fact Greencoat UK Wind’s dividend has risen in line or ahead of inflation each year since IPO in 2012. Based on its annual dividend target of 10.70p for 2026, the quarterly dividend-payer offers an attractive yield of 10.3%.

With £4 billion in assets, Greencoat UK Wind is the largest trust in the AIC Renewable Energy Infrastructure sector. The benefits of scale allow the manager to levy the lowest ongoing charge among the peer group at 0.83%.

iShares Global Clean Energy Transition (INRG)

| Share price: 907p | Total assets: £3.25 billion |

| Total expense ratio: 0.65% | Dividend Yield: 0.86% |

Source: BlackRock

The iShares Global Clean Technology Transition (LON:INRG) fund aims to track the return of the S&P Global Clean Energy Index. Unlike the two trusts, the fund’s focus is on capital growth rather than income, although it does pay quarterly dividends.

After four years of back-to-back losses, reflecting investor antipathy towards renewables, the fund has sparked into life in 2026. Year-to-date it has returned 46%, although that still leaves it almost 40% down on 2021.

In other words, there is still an awful lot of catching up to do and the fund has the wind in its sails. By geography, the fund is heavily weighted to the US, followed by three of the four BRICs, China, Brazil and India.

By sector, Industrials and Utilities make up around 70% of the portfolio with Technology making up most of the rest. Therefore, by geography and by sector the fund is a useful diversifier in any portfolio which is mainly UK-weighted.