FTSE 250 Trustpilot (TRST) delivered one of its strongest financial performances to date, with annual operating profit more than quadrupling. AI‑driven search activity fuelled explosive new traffic growth. The online reviews platform, already a major digital presence, has rapidly become one of the most frequently cited data sources for large language models. Moreover, this is reshaping its strategic position in the global tech ecosystem. Trustpilot is fast emerging emerging as ‘an AI winner.’

Having flagged the results as ones to watch last Friday (read here), they did not disappoint. The stock surged 26% in early London trading following Tuesday’s announcement. Investors reacted to what RBC analysts described as ‘a very strong set of results’. There was also clear evidence that Trustpilot is emerging as ‘an AI winner.’

| Trustpilot (TRST) | Price: 222.80p (+26.5%) | Market cap: £864.86m |

AI drives unprecedented traffic surge

At the centre of Trustpilot’s breakout year was a remarkable 1,490% year‑on‑year increase in traffic from AI‑powered search tools. Review‑driven answers from ChatGPT, search engines and other LLM‑based systems increasingly referenced Trustpilot’s vast library of user‑generated reviews. According to Promptwatch, the platform ranked as the fifth most‑cited website on ChatGPT globally in January.

The structural benefit is clear: as artificial intelligence tools scale, platforms with large, clean, and trusted datasets stand to gain disproportionately. Trustpilot’s data footprint positions it alongside other digital platforms—such as Reddit (RDDT) and Stack Overflow. These platforms have seen surging demand for training‑grade information from AI developers.

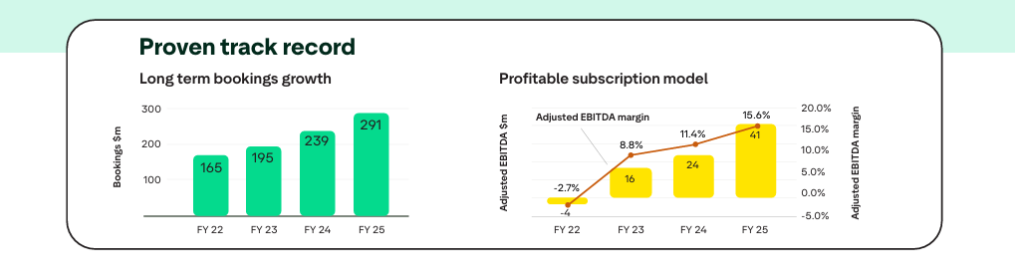

Trustpilot reported $16 million in operating profit for 2025, up from $3.8 million a year earlier—a 320% increase driven by improved monetisation, operational leverage, and the surge in inbound AI‑related traffic. Furthermore, earnings were up more than 400% on an adjusted basis.

Guidance strengthens

Looking ahead, management forecast high‑teens revenue growth in 2026, with a further 2%-3% point expansion in adjusted EBITDA margins. Strong bookings in 2025 provide early visibility into continued commercial momentum.

RBC expects ‘material consensus upgrades’. They argue that Trustpilot’s expanding prominence in AI citation data mirrors the platform’s growing influence on digital consumer decision‑making.

Despite the strong results, Trustpilot continues to rebut allegations raised in December by US short‑seller Grizzly Research. Grizzly Research accused the company of creating fake accounts to pressure firms into paid plans. Trustpilot has categorically denied the claims.

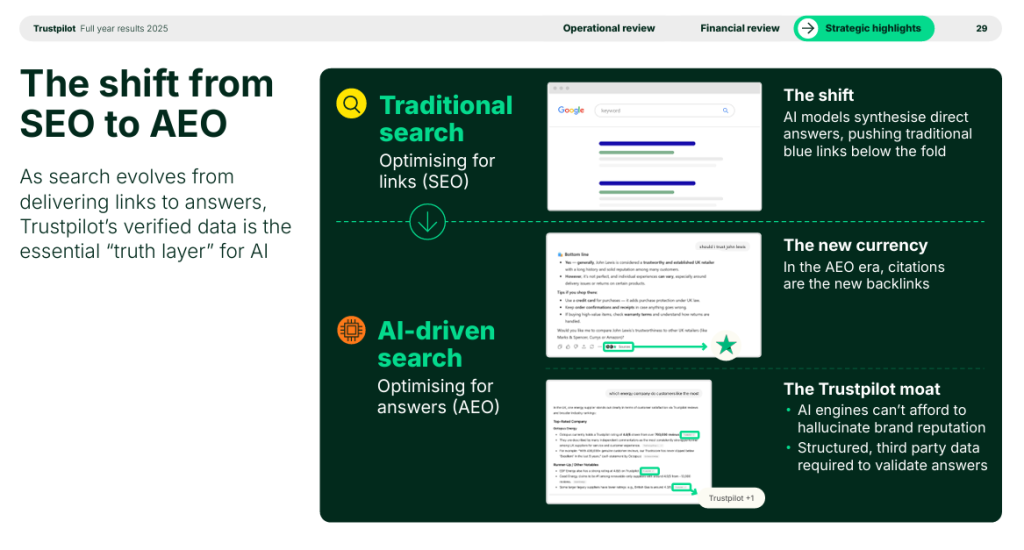

The numbers tell a clear story: Trustpilot is no longer just a reviews platform. In the AI era, it is becoming a foundation data supplier. Its content increasingly powers the very systems shaping global search and digital commerce.

This is crucial as we move from the SEO world and into the AEO adoption age, or search engine optimisation to answer engine optimisation. Along that journey, key investment quality metrics like returns on capital and margins are shifting. These are going from promising to powerful.

Disclaimer: The author Steven Frazer has a personal interest in Trustpilot.

You might also like: