The Scottish Mortgage Investment Trust (SMT) wants to up its exposure to ambitious private companies. The global growth fund is one of the most owned by retail investors. It will gather shareholders at the offices of broker Deutsche Numis on 10 April 2026. They will vote on a proposal to expand its assets allocation to unlisted businesses.

Under existing rules, the trust cannot allocate more than 30% of its total assets to private companies, calculated at the time a new investment is made. It’s a guardrail designed to balance boldness with prudence.

Shifting arithmatic

For years, Scottish Mortgage has been known for its willingness to back ambitious private companies long before they reach public markets. But that same long‑term conviction has brought it close to the boundaries of its current investment policy.

| Scottish Mortgage (SMT) | Price: £11.955 (+1.14%) | Market cap: £13.04bn |

Yet the arithmetic has been shifting. Over 2024 and 2025, Scottish Mortgage carried out roughly £3 billion of share buybacks. This reduced its base of publicly traded holdings, because those buybacks were largely financed by selling listed shares. At the same time, some of the trust’s most promising private investments have gained value.

SpaceX, the standout example, surged in value following a December 2025 valuation update, jumping to $800 billion. Its previous funding round a year earlier set a valuation at $350 billion. In February 2026, the Elon Musk-led firm raised further funding as part of its merger with xAI. This set a $1.25 trillion valuation.

SpaceX is believed to be eyeing an IPO on Wall Street, rumoured for June, with a $1.75 trillion valuation. Scottish Mortgage’s stake in Space X has jumped from about 8.2% to 15.4% currently. This is more than half of its entire private portfolio allocation.

Need for flexibility

These forces, both deliberate and market‑driven, have pushed the trust’s private‑company exposure toward the upper limits of its policy.

The trust plans to ask shareholders for greater flexibility, including permission to invest up to an additional £250 million in private businesses during periods when the 30% threshold is exceeded. This would not be a permanent expansion of its mandate; the authority would have to be renewed every year starting in 2027. Nor is it an open‑ended allowance – the extra capacity amounts to around 1.7% of total assets.

SMT’s top five private company stakes

| Private company | % of assets |

| SpaceX (aerospace and AI) | 15.4% |

| Bytedance (social media) | 4.1% |

| Stripe (digital payments) | 3.9% |

| Zipline (delivery drones) | 2.0% |

| Sea (ecommerce, gaming) | 1.9% |

Source: Scottish Mortgage

In essence, the board is looking to ensure it can continue supporting high‑growth private companies—even during temporary moments when accounting boundaries tighten. Should shareholders reject the proposal, Scottish Mortgage will simply continue under the existing rules. This would mean no new private investments could be made if exposure remains above 30%.

Making your decision

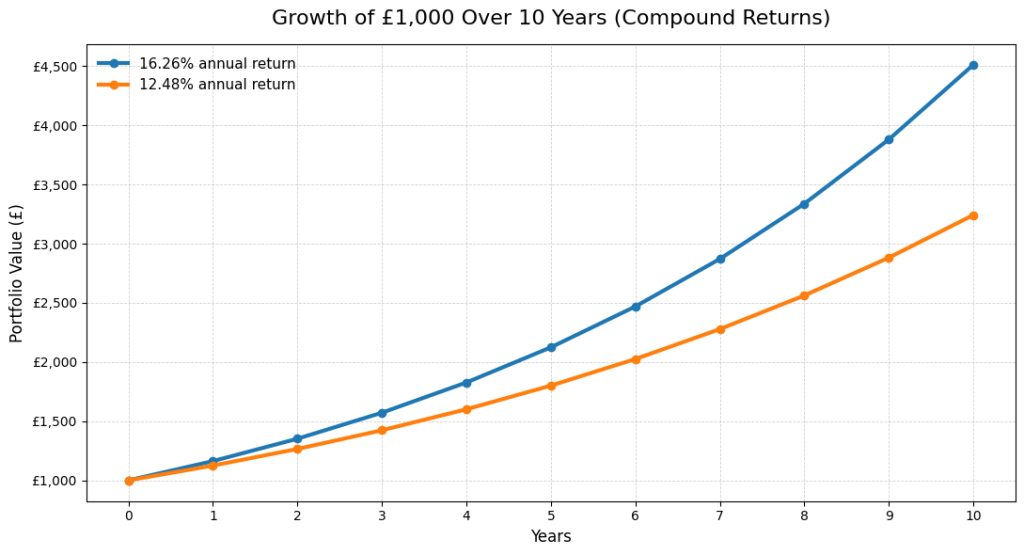

Coming to a decision requires investors to consider the long-term track record of Scottish Mortgage, which is nothing short of outstanding. Over the past decade, it has delivered total returns (income and capital growth combined) that average 16.26% a year. This places it in the top 1% of all trusts, according to Morningstar data. It has comfortably outpaced its global growth index.

That effectively means, £1,000 invested in the trust over the past 10 years would now be worth £4,511.32. By contrast, this would be £3,241.55 based on index performance.

Over 15 years, a timeframe that roughly tallies with when Scottish Mortgage manager Tom Slater joined the trust. The outperformance is far greater, turning £1,000 into £9,569.61 versus £4,606.71 for the index.

The decision is straight-forward for this shareholder, who is very happy to back Tom Slater and his team, and vote yes.

Disclaimer: The author Steven Frazer has a personal interest in Scottish Mortgage.

You might also like: