To quote the firm’s advertising slogan, with think Marks & Spencer (MKS) shares are ‘Remarksable’ value at their current price.

| Share price: 347p | Current P/E: 15x |

| Market Cap: £7.1bn | Current yield: 1.3% |

| Sector: Food Retail | FY end: March |

ALL TO PLAY FOR

M&S is one of the UK’s most-loved brands, yet the business has managed to change its spots dramatically over the past decade.

Where once it was largely a clothing and homewares retailer, it is now one of the nation’s smartest food stores.

Including its 50% holding in Ocado Retail, which is fully consolidated for the first time this year, Food sales make up around 75% of group revenue.

Fashion, Home and Beauty (FHB) sales make up around 20% of the total, while the rest comes from the group’s overseas joint ventures.

In April 2025, the group suffered a major cyber incident which seriously affected trading.

In-store Food sales, online FHB sales, the Click & Collect service and order deliveries all suffered.

However, thanks to the underlying strength of the business and its firm financial foundations M&S has already bounced back.

Now the focus is to keep growing faster than the market in both Food and Non-Food while improving margins.

As chief executive Stuart Machin said at the interim results, the firm has made meaningful progress in recent years.

There is still much to do, though, and there are still plenty of opportunities ahead so it’s ‘all to play for’.

FY2025 revenue by division

| Food (£m) | 9,021 | 64.8% |

| Fashio, Home & Beauty (£m) | 4.235 | 30.4% |

| International (£m) | 658 | 4.8% |

Source: Marks & Spencer

SOLID FINANCIAL FOOTING

M&S ended the financial year to March 2025 with net debt of £1.79 billion, a reduction of £376 million.

This was driven by free cash flow generation, which allowed for the repurchase of certain bonds, and a change in the recognition of the Scottish Limited Partnership liability.

The group had liquidity of £1.74 billion, comprising cash and equivalents of £864 million and undrawn banking facilities of £875 million.

Meanwhile, net assets were £2.95 billion, an increase of around 4% due to lower borrowing.

This strong financial position means M&S can focus on growing its food store estate this year, including investing in a number of former Homebase sites.

More than 14 new food stores are expected to open this year, and over 50 are currently approved for opening alongside several extensions.

The group has also invested £340 million investment in a new 1.3m square foot national distribution centre in Daventry due to open in 2029.

CYBERATTACK DENTS FORECASTS

At the start of the current financial year in April 2025, M&S was hit by a sophisticated cyberattack which took down many of its systems.

The firm estimated the cost of the attack at around £300 million in terms of operating profit before mitigation efforts.

In its results for the 1H to September 2025, the company reported a drop in adjusted pre-tax profit of £229 million.

This was directly due to lower online sales, increased stock management costs in FHB and higher markdowns and waste in Food.

Part of the impact was offset by insurance, but the firm also had £50 million of higher costs for higher NI contributions and a new packaging levy.

The Food business has now largely recovered, while the rebound in FHB has been slower due to reduced stock availability and fewer store visits, partly due to the absence of click and collect.

FY26-FY28 consensus estimates

| FY26E | FY27E | FY28E | |

| Revenue (£m) | 17,400 | 18,800 | 19,800 |

| Operating profit (£m) | 1,430 | 1,750 | 1,820 |

| Operating margin (%) | 8.2 | 9.3 | 9.2 |

| Pre-tax profit (£m) | 655 | 975 | 1,050 |

| EPS (p) | 23.4 | 33.3 | 36.8 |

| DPS (p) | 4.3 | 5.2 | 6.2 |

Source: Marks & Spencer, data as of 20 October 2025

POSITIVE RECENT TRADING

For the 13 weeks to 27 December, M&S posted 3.3% sales growth excluding Ocado Retail with Food up 6.6% and FHB down 2.5%.

Weak FHB sales weren’t a surprise as the firm had said it would discount old stock to make way for new ranges.

Ocado Retail sales up 13.7% were a pleasant surprise, by contrast, with M&S brands now making up a third of turnover.

Yet analysts haven’t upgraded their forecasts, which means they are still where they were in October 2025.

This is likely the market building in a ‘margin of safety’ for further potential downside from the cyberattack or for management execution.

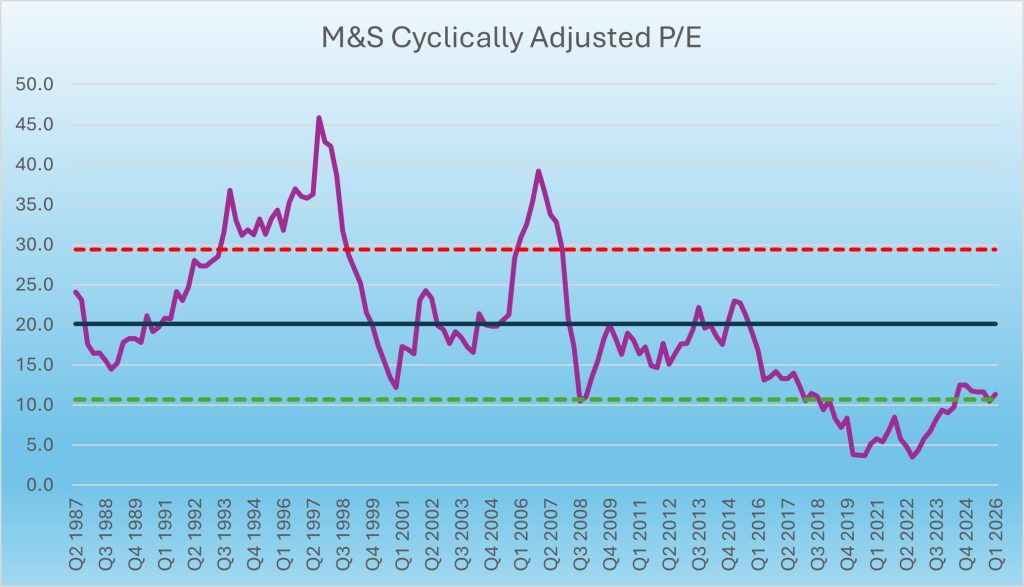

AN ATTRACTIVE VALUATION

Turning to valuation, the shares currently trade around 350p which is roughly where they were last summer.

Meanwhile, it looks like earnings forecasts for FY26 and FY27 have been pushed back 12 months.

Therefore, analysts now see EPS of 33.3p in FY27 instead of FY26 and EPS of 36.8p in FY28.

Based on these forecasts, if the shares revert from their current 15 times depressed earnings to their cyclically-adjusted mean of 20 times ‘normal’ earnings by March 2028, we envisage a price of 736p or more than double the current level.