Smithson Investment Trust (SSON)

| Price: £15.76 | NAV/share: £16.20 |

| Market Cap: £1.7bn | Discount to NAV: -2.8% |

| Current Yield: 1.3% | OCF: 0.9% |

Source: Smithson. Data correct as of 18 December 2025

The board of Smithson investment trust has proposed changing from a closed-end to an open-ended structure. We explain the rationale, the process and why investors should back the board’s proposal.

Fund Strategy

Smithson invests in shares issued by small- and mid-sized listed companies globally with a market capitalisation at the time of initial investment within the range of the constituents of the MSCI World SMID Index.

The fund is a long-term investor in its chosen stocks and does not adopt short-term trading strategies. It invests in approximately 25 to 40 companies.

The Proposal

On 12 November 2025, Smithson’s board announced it would seek permission from shareholders to convert from a closed-end to an open-ended structure to restore value for investors.

The proposal was backed by US investor Saba Capital and Fundsmith founder Terry Smith.

The new open-ended fund, Smithson Equity, will trade at NAV (net asset value) on a daily basis and there will be no dilution for shareholders who roll their investment into it, so £100 invested in the trust becomes £100 invested in the new fund.

Smithson Investment Trust (SSON)

UK shareholders who roll their investment into the fund may also do so without triggering a charge for capital gains even if they hold the shares outside a tax-efficient wrapper such as a SIPP or an ISA.

Smithson Equity will continue to be managed by Simon Barnard and will continue the strategy of investing in small- and mid-sized listed companies to deliver long-term capital appreciation.

Background to the proposal

Funds and investments trusts are an important part of the UK stock market and can be a useful way for investors to diversify their portfolios.

One advantage of trusts, thanks to their closed-end structure, is they are able to put aside excess earnings when they have a good year and build up a reserve which can be used to top up dividends in less good years.

However, for some time the UK investment trust sector has suffered from large discounts to NAV (net asset value) meaning their shares trade at less than the overall value of their portfolios excluding any debt or ‘gearing’.

According to the AIC (Association of Investment Companies), the average discount to NAV in November 2025, excluding FTSE 100 private equity firm 3i GROUP (III), was 14.2%, while the average performance over one year was 13.6% compared with 16.7% for the FTSE All Share.

In the case of Smithson, which has assets of £1.7 billion, the discount to NAV at the start of November was 9% based on a share price of 1,546p and a net asset value of 1,698p/share.

Although the discount was smaller than average, it wasn’t that different to April 2022 when the board embarked on a share buyback totalling almost £1 billion, representing 70 million shares or close to 40% of the issued capital.

Source: Trustnet. Data correct as of 18 December 2025

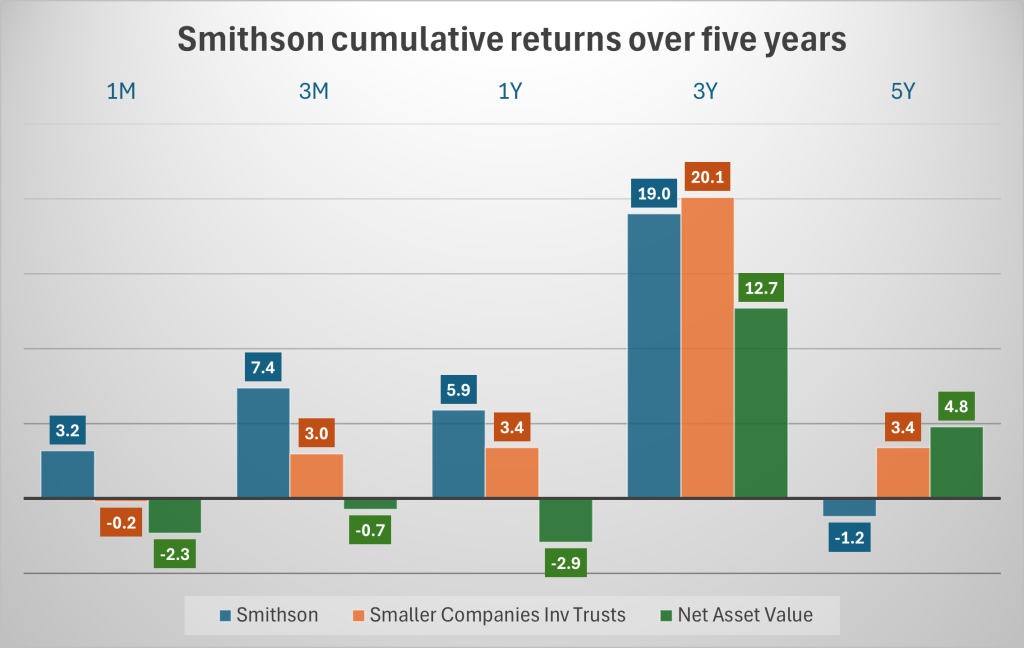

Performance

Shortly after UK interest rates began to rise in 2022, Smithson’s style of investing – buying and holding high-quality companies and compounding their earnings over the long term – fell out of favour, with the market preferring cheap, unloved UK companies on the one hand and highly-priced US technology companies on the other.

Over the past year, however, investors have broadened their horizons and once again begun to appreciate the attractions of superior long-term cash-flow and earnings growth.

As a result, Smithson shares have performed better and over the last 12 months have outperformed the AIC’s Smaller Companies benchmark.

Source: Trustnet. Data correct as of 4 December 2025

Portfolio

The trust doesn’t reveal individual weightings for its holdings on a monthly basis, but it does publish its top 10 positions.

Top fund holdings as of 18 December 2025

Diploma

Moncler

Qualys

Recordati

Rational

Spirax Group

Vertiv

MSCI

Rollins

Oddity

Source: Smithson

Investors will no doubt recognise UK firms DIPLOMA (DPLM) and SPIRAX (SPX) as typical examples of high-growth, high-quality ‘compounders’ with an impressive track record of value creation.

What investors should do next

For the time being, shareholders should do nothing as the process of gaining FCA approval and setting up the new open-ended investment company may take until the end of January.

Once that has been achieved, a circular will be sent outlining the proposal in more detail and proposing two shareholder meetings: the first, to approve the terms of the proposal, and the second, to approve the voluntary liquidation of the trust and transfer of the assets to the new fund.

At that point, shareholders will have the option of rolling their investment into the fund or realising some or all of their holding for cash at minimal cost.

Our View

We believe investors should back the board’s bold approach, which is designed to do away with the problem of the discount once and for all, and roll their holdings into the new fund, sticking with the manager and the well-understood strategy.

While other trusts have resisted attempts by activists to tackle their discounts, ‘pulling up the drawbridge’ to defend themselves, the board of Smithson has been open to suggestions on behalf of all investors, and we can envisage other trusts following the same path as it offers a neat solution to the problem of persistent discounts.

Admittedly the strategy of owning a concentrated portfolio of high-quality growth companies which can compound their earnings has been out of favour in recent years, but we have no doubt it is the right one for investors looking to build wealth over the long term and it should be well suited to the new structure.

We also believe the tide has turned in favour of small- and mid-cap companies, particularly in the UK, and this is the right time to be investing for the future. As a footnote, the board’s proposal has been well received by the market with Smithson’s discount to NAV narrowing from around 9% to just 2.8% as of the middle of December.

Disclaimer

All information used in the publication of this report has been compiled from publicly available sources which are believed to be reliable, but Sharesify.com does not guarantee the accuracy or completeness of this report and has not sought for it to be independently verified.

Opinions contained in this report represent those of Sharesify.com at the time of publication, and any forward-looking statements are based on assumptions and/or forecasts of future results which involve known and unknown risks and uncertainties which may cause the actual results to be materially different from current expectations.

No personalised advice: Information provided in this report should not be construed in any way as personalised advice or as an offer or solicitation to effect a transaction in any security.

This communication is being distributed in the United Kingdom and is directed only at:

(i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended

(ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and

(iii) persons to whom it is otherwise lawful to distribute it.

The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document.

Exclusion of Liability: To the fullest extent allowed by law, Sharesify.com shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note.

Investment in securities mentioned: Sharesify.com does not conduct any investment business and does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of the company may have a position in any or related securities mentioned in this report, subject to the company’s policies on personal dealing and conflicts of interest.

Copyright 2025 Sharesify.com

Disclaimer: This content is for information only and is not investment advice. Always do your own research before investing. Click here to see full disclaimer.