TSMC (TSM), or Taiwan Semiconductor Manufacturing Company, is entering its upcoming earnings season with renewed momentum. If you are looking for further evidence of the Taiwanese chip firm’s central role in the global AI boom, here it is.

The world’s largest contract chipmaker reported a sharp surge in March revenue. This highlights how demand for advanced AI-related chips is reshaping its growth profile. Moreover, it reinforces investor expectations ahead of Q1 earnings report on 16 April.

| TSMC (TSM) – US ADRs | Price: $365.49 | Market cap: $1.58tn |

March revenue jumped 45.2% year-on-year to NT$415.19 billion, while also rising 30.7% from February. That strong finish lifted Q1 revenue to NT$1.13 trillion, slightly ahead of market expectations. It was also significantly higher than the NT$839.25 billion recorded a year earlier.

Deep AI exposure

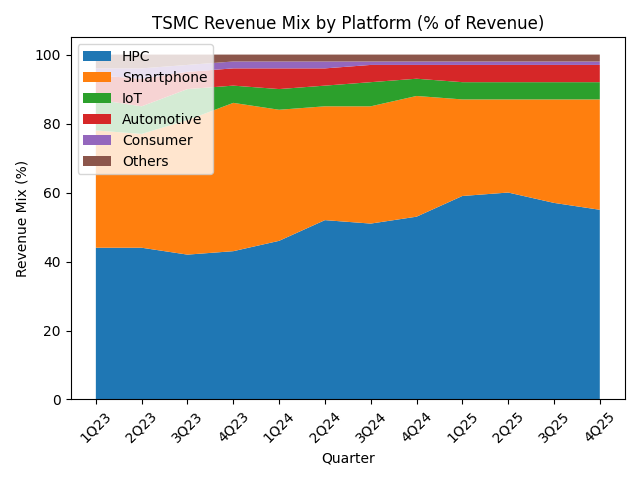

The acceleration reflects TSMC’s deep exposure to customers building out AI and cloud infrastructure, including key relationships with Nvidia (NVDA) and other leading AI chip designers. While TSMC remains a major supplier to smartphone makers and consumer electronics firms — most notably Apple (AAPL) — AI-related processors have increasingly become the dominant contributor to growth.

That shift is not only driving near-term revenues but also reshaping longer-term expectations. TSMC shares have more than doubled over the past year as earnings expanded alongside surging AI demand. This is a trend Wall Street expects to persist.

Source: TSMC

Goldman Sachs recently identified TSMC as a standout beneficiary of structurally rising AI workloads. The bank argues that strength in high-performance computing will more than offset lingering softness in consumer electronics.

The bank raised its earnings forecasts for 2026 and 2027 by 4% to 6% and introduced estimates for 2028. It is projecting revenue growth of 35%, 30%, and 29% over the 2026–2028 period. EPS is now expected to rise to NT$95.24 in 2026 and NT$125 in 2027.

Demand and margin expansion

Goldman’s analysts point to robust demand for AI accelerators, GPUs, and AI-focused server CPUs as the primary growth engines. This is supported by a structurally tighter supply environment for leading-edge manufacturing.

Crucially for investors, Goldman expects margins to expand alongside this demand. Leading-edge chip capacity is likely to remain constrained through at least 2027. Furthermore, a richer product mix tilted toward advanced nodes should lift profitability. Gross margins are forecast to climb from 64.2% in 2026 to 66.5% by 2028, aided by productivity gains and higher utilisation.

To support this growth, TSMC is also expected to ramp up capital spending aggressively. Goldman now projects capital expenditure of roughly $200 billion between 2026 and 2028 as the company invests heavily in next-generation process technologies. Together, strong near-term revenue momentum and improving long-term visibility reinforce the view that TSMC is not only riding the AI wave—but helping define its industrial foundation.

You might also like: