Semiconductor technology supplier Applied Materials (AMAT) saw its stock surge around 12% in after-hours trading thanks to the accelerating AI investment wave. The near-$300 billion company’s Q1 2026 results comfortably beat market expectations. Moreover, these results underscore the growing strength of AI-driven chip demand.

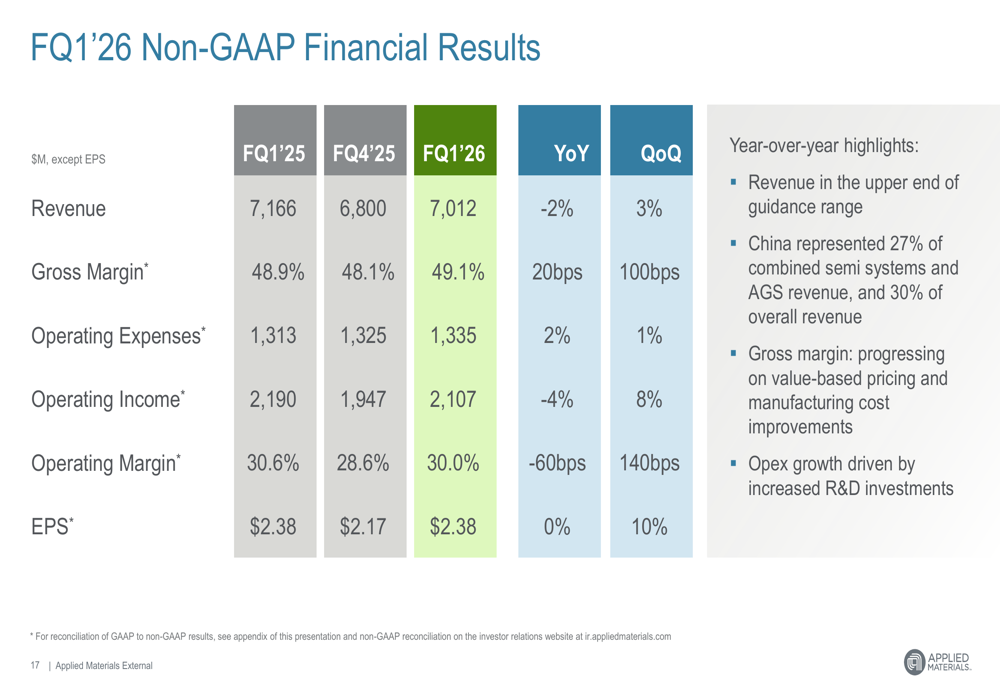

The Santa Clara-based company reported Q1 non-GAAP earnings per share of $2.38, ahead of the $2.21 consensus estimate, on $7.01 billion revenue, which also topped Wall Street projections ($6.87 billion).

| Applied Materials (AMAT) | Price: $368.24 (+12%) | Market cap: $292bn |

Record revenues

Performance was supported by record activity across key business lines. The Semiconductor Systems division posted an all-time high in DRAM-related revenue, or Dynamic Random Access Memory. Moreover, its Applied Global Services segment also delivered record sales in services and spare parts. This reflects continued high utilisation rates of customers’ installed tool bases. In fact, the results underscore the growing strength of AI-driven chip demand in multiple segments.

CEO Gary Dickerson said the results reflected a structural shift in industry spending patterns. He explained that AI computing is now acting as a major catalyst for semiconductor capital investment. No shock there.

He added that the company expects its semiconductor equipment business to expand by 20%+ during the current calendar year. This signals strong demand visibility across memory and logic markets. Moreover, these results underscore the growing strength of AI-driven chip demand throughout the sector.

Upscaling to meet demand

Management also emphasised ongoing efforts to scale production capacity to support next-generation chip manufacturing. CFO Brice Hill said the company has nearly doubled system manufacturing capability in recent years. In addition, it has strengthened supply chain resilience and built inventory buffers to position for continued market expansion.

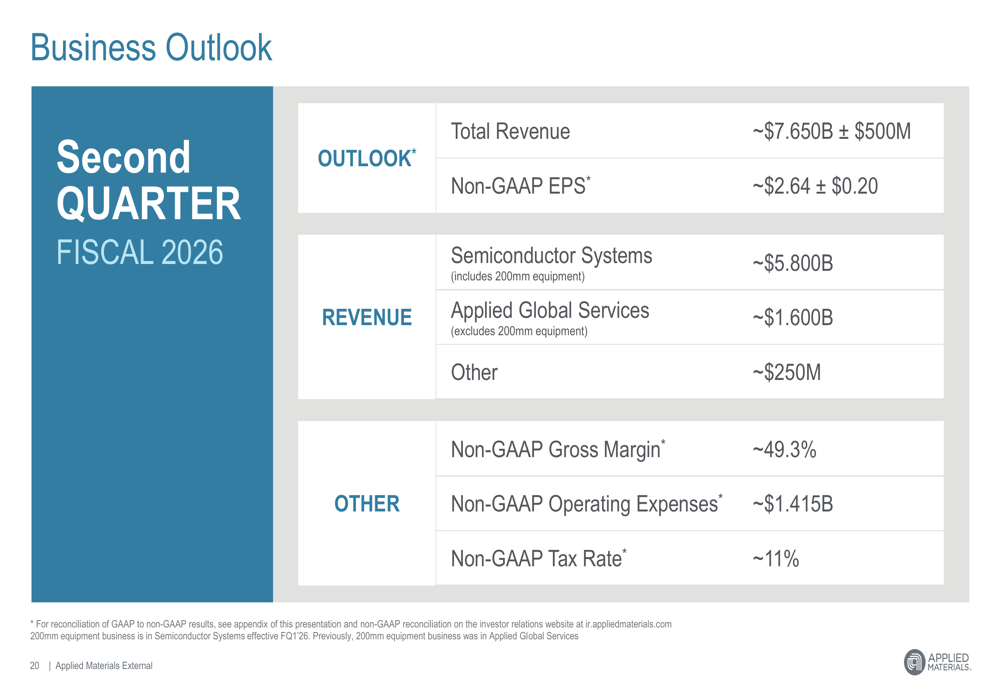

Looking ahead, Applied Materials issued upbeat Q2 fiscal 2026 guidance. It forecast revenue in the range of $7.15 billion to $8.15 billion. The midpoint of that range sits well above the current analyst consensus of around $7 billion. This suggests continued momentum across semiconductor capital equipment markets as AI-related investment cycles accelerate. Notably, the results underscore the growing strength of AI-driven chip demand for the coming quarter.

The results reinforce the view that semiconductor equipment suppliers remain among the most direct beneficiaries of the global AI infrastructure build-out. Moreover, chipmakers expand fabrication capacity to support rapidly rising compute demand.

Another chip tech company beats ‘The Street’. Although estimates for AMAT were pitched low, Koyfin consensus data shows low-single-digit growth was pencilled in for fiscal 2026 in revenue/EPS. However, forecasts are likely to upgrade over the coming days.

Analysts at Summit Insights see plenty of scope for AMAT outperformance over consensus this year. This is something the company has pulled off in 13 of its past 14 quarters.

With operating margins, ROE and ROCE metrics running at around 30%-35%, you can see why AMAT has been backed by many of the UK’s most popular funds and investment trusts.

You might Also like: