Asian equities traded mixed on Friday but remained on course for sharp weekly losses, as escalating conflict in the Middle East and a spike in oil prices rattled investor sentiment across global markets.

US equity futures were broadly flat during Asian hours, offering little relief after Wall Street extended losses overnight amid rising geopolitical tension and higher Treasury yields.

Geopolitical Shock

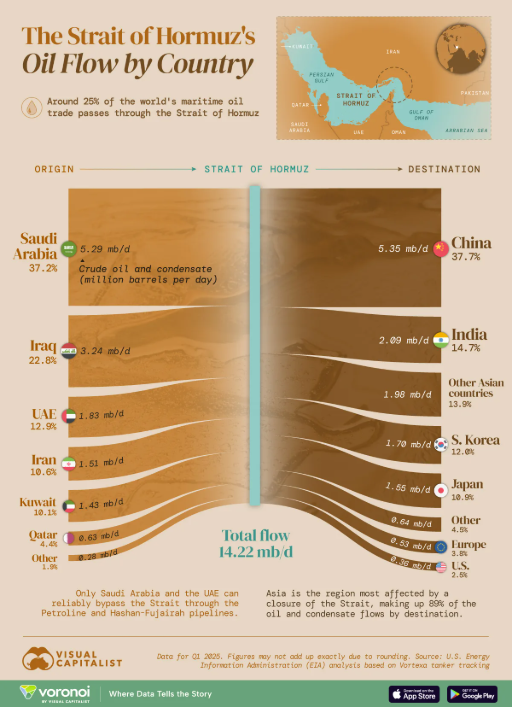

The conflict involving Iran, Israel and the United States entered its seventh day on Friday, with no indication of de-escalation. Analysts warn that continued instability could disrupt energy flows through the Strait of Hormuz, a critical chokepoint that handles roughly 20% of global oil supply, a topic we discussed briefly on the Sharesify podcast earlier this week (listen here).

Source: Visual Capitalist

Oil markets priced in the elevated geopolitical risk aggressively:

- Crude prices surged more than 15% this week, the steepest jump in months

- Energy-importing Asian economies saw the sharpest market fallout

South Korea’s KOSPI was particularly hard-hit—down 1% on Friday and on track for a 12% weekly plunge, its worst five-day drop since the pandemic-era volatility.

Japan’s Nikkei 225 managed a modest 0.6% gain, but still headed for a 6% weekly decline, reflecting global aversion to risk assets. China’s Shanghai Composite and CSI 300 indices were each poised to lose more than 1% for the week, weighed down by weak domestic demand and external shocks.

Hong Kong’s Hang Seng rose 2%—a rare bright spot—but still faced a 3% weekly fall, demonstrating the broad risk-off tone across the region.

India’s Nifty 50 edged lower and was on track for a 2% weekly decline.

Oil Surge Rekindles Inflation Concerns Globally

The spike in crude prices has renewed concerns about global inflation, complicating the policy path for central banks already grappling with uneven economic data.

Higher energy costs traditionally feed into:

- Transportation prices

- Manufacturing input costs

- Consumer inflation

This dynamic may delay potential interest-rate cuts—particularly in the US, where rising bond yields and market volatility already point to nervousness about the economic outlook.

Investors are now awaiting the US February nonfarm payrolls report, due later Friday, which could influence expectations for Federal Reserve policy in the coming months.

Volatility Set to Persist

With geopolitical tensions high, oil prices elevated, and monetary policy uncertainty building, analysts expect continued volatility across global equities.

Asian markets, heavily exposed to energy costs and global supply-chain risks, may remain under pressure unless there is:

- A de-escalation in Middle East tensions

- Stabilisation in crude prices

- Clearer forward guidance from central banks

For now, the risk-off mood remains dominant as investors brace for another turbulent trading week.

You might also like: