")

")

Broadcom delivered a robust fiscal 2026 Q1 performance (to end Jan), beating Wall Street expectations across revenue, earnings, and forward guidance. The results underscore Broadcom’s strengthening position as a key supplier of custom AI silicon, particularly for hyperscale cloud providers seeking alternatives to Nvidia (NVDA)-built solutions.

The company also announced a share buyback plan of up to $10 billion.

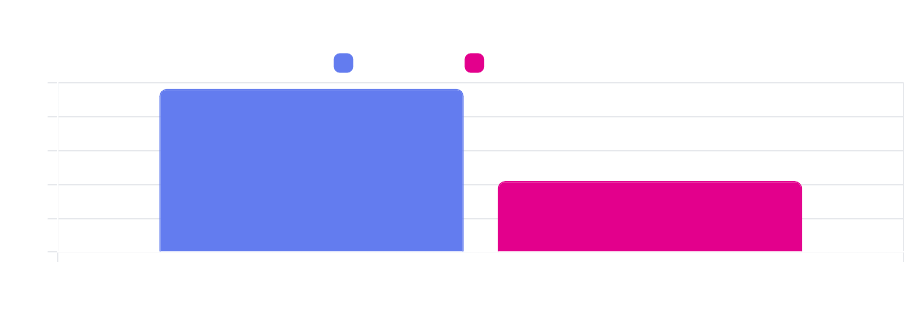

In Q1 2026 (webcast here), Broadcom generated earnings of $2.05 per share on an adjusted basis on revenue of $19.31 billion. Analysts had expected EPS of $2.02 on revenue of $19.21 billion.

| Broadcom (AVGO) | Price: $337.65 (+6.3%) | Market cap: $1.606tn |

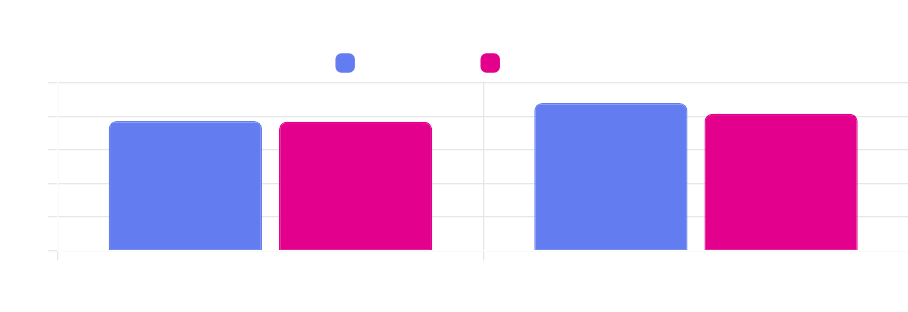

The chip designer said it expects Q2 2026 revenue to be about $22 billion, compared to a consensus estimate of $20.4 billion. AI semiconductor revenue is expected to be $10.7 billion, implying QoQ growth of .

‘Broadcom achieved record Q1 revenue on continued strength in AI semiconductor solutions. Q1 AI revenue of $8.4 billion grew 106% YoY, above our forecast, driven by robust demand for custom AI accelerators and AI networking’, CEO Hock Tan said in a statement.

Earnings summary

| Metric | Reported | Consensus | Surprise |

| Adjusted EPS | $2.05 | $2.02 | +1.5% |

| Revenue | $19.31bn | $19.21bn | +0.5% |

| AI Semiconductor Revenue | $8.4bn | Internal forecast beat | +106% YoY |

Broadcom stock rallied more than 6% in pre‑market trading after the announcement, further supported by the company’s $10 billion share buyback plan.

Revenue breakdown

Key takeaways:

- AI revenue of $8.4 billion works out at ~44% of total company revenue.

- AI semiconductor revenue more than doubled year‑on‑year, highlighting accelerating demand for custom ASICs and networking.

- Total revenue of $19.31 billion was a company record for a Q1.

Forward guidance signals momentum

Broadcom issued better‑than‑expected guidance for fiscal Q2:

- Expected revenue: $22 billion

- Analyst consensus: $20.4 billion → Broadcom is guiding nearly 8% above expectations.

The company anticipates $10.7 billion in AI semiconductor revenue for the quarter, a sign of rapid scaling across its accelerator and AI networking product lines.

Strategic industry position

Broadcom continues to gain recognition as a viable alternative to Nvidia in the custom silicon market, especially for hyperscalers such as:

- Alphabet (GOOG)

- Meta Platforms (META)

Analyst at Jefferies highlighted that Broadcom’s ASIC (application-specific integrated circuit) solutions have transitioned from ‘second source’ to true competitive alternatives, especially for Google’s externally sold custom chips.

Broadcom operates across:

- AI accelerators

- Networking connectivity

- Wireless components

- Server/storage silicon

- Infrastructure software (private cloud, cybersecurity, enterprise software)

This diversified, high‑margin portfolio supports consistent cash flow and large-scale capital returns. Broadcom returned $10.9 billion to shareholders in Q1 through $3.1 billion of cash dividends and $7.8 billion of stock repurchases.

Net debt, a metric Sharesify said was worth watching in our podcast, came in at ~$50 billion, versus $79.9 billion shareholders equity. That puts gearing at ~62.5%, comfortable for a company throwing off a $8 billion in free cash flow, +33% in the quarter,

Market context

The earnings come during a period of increased scrutiny on AI spending. Investors are now distinguishing between what they currently see as AI winners (chip designers, hyperscaler infrastructure), and AI losers (software sub-sectors facing disruption), although how accurate that will prove to be, only time will.

Despite Nvidia also delivering strong results last week, the stock remained pressured by concerns around capital expenditure sustainability, macro demand visibility, and AI project ROI (return on investment) timelines. Jefferies’ analyst Blayne Curtis noted that both Nvidia and Broadcom are trading at ‘depressed multiples’ despite being the most likely long-term AI beneficiaries.

‘We have line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027’, Broadcom CEO Hock Tan said on a conference call with analysts. ‘We have also secured the supply chain required to achieve this.’

Investment prospects

Bull case drivers

- Explosive growth in ASIC-based custom AI accelerators

- Strong Q2 guidance indicating continued demand inflection

- Increasing share among hyperscalers seeking alternatives to Nvidia

- Diversified revenue streams stabilising earnings

- Aggressive capital return programmes

Risk factors

- Broader tech-sector sentiment on AI spending

- High concentration of revenue growth from a few cloud megacaps

- Macro environment uncertainty affecting capex cycles

Conclusion

Broadcom’s Q1 2026 performance and Q2 guidance confirm its status as a structural AI leader, and investors appear to appreciate that right now. With AI revenue doubling YoY and hyperscalers embracing Broadcom’s ASIC roadmap, the company is positioned for sustained growth throughout fiscal 2026 and 2027.

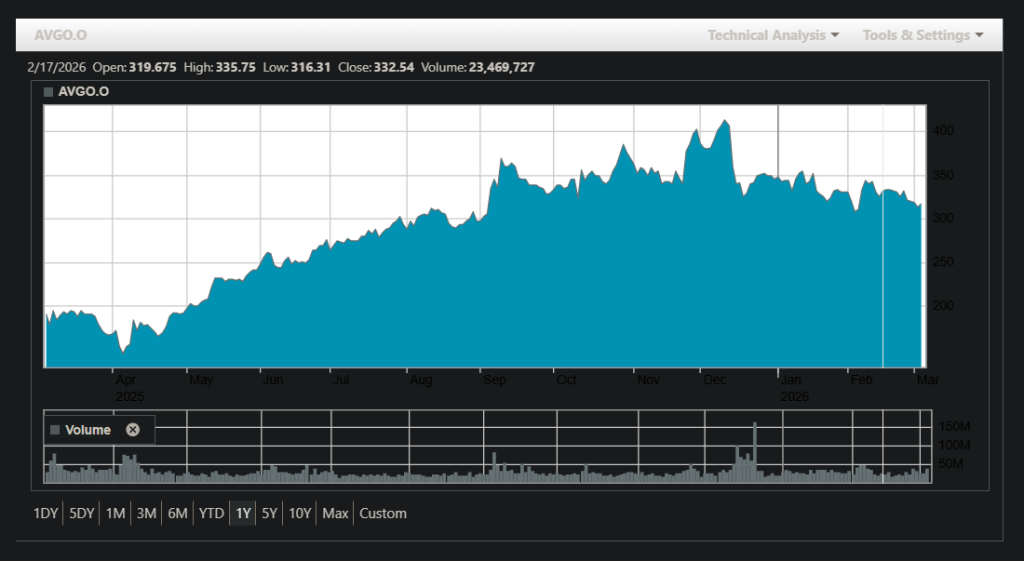

Broadcom stock 1-year performance

Source: Broadcom, LSEG

Following the results, analysts at Citi, Baird, Rosenblatt and RBC Capital all raised forecasts and share price targets, the latter’s range now extending from $335-$575, putting the 12-month average at $454, based on Koyfin data.

Despite sector-wide volatility, Broadcom’s combination of strong fundamentals, accelerating AI silicon demand, and a sizable buyback program presents a compelling long-term investment narrative.

Disclaimer: The author Steven Frazer has a personal interest in Broadcom.

You might also like:

")