Cloudflare (NET) delivered a clear beat in Q4 2025 overnight sparking a huge surge for the stock. The share price jumped nearly 16% after the cybersecurity firm posted $614.35 billion Q4 revenue, 34% above analyst projections.

| Cloudflare (NET) | Price: $208.27 (+15.7%) | Market cap: $72.9bn |

Non-GAAP (Generally Accepted Accounting Principles) EPS of $0.28 also nudged beyond expectations of $0.27, a big jump on $2024’s $0.19.

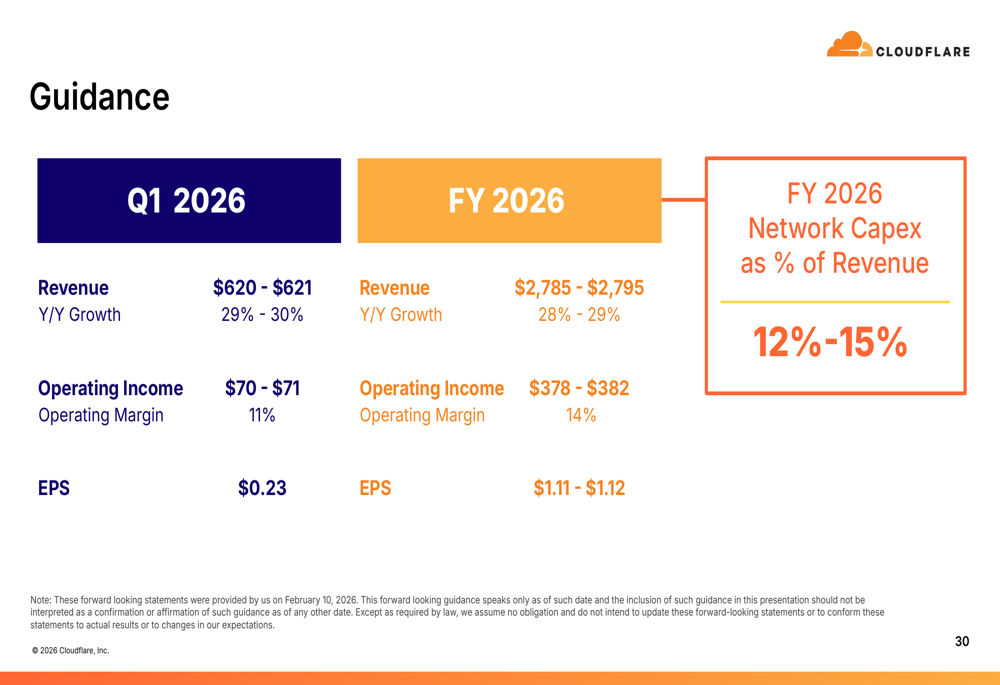

Guidance above forecast

Guidance was also upbeat. Cloudflare is forecasting a revenue midpoint of $2.79 billion for full year 2026, above the current analyst consensus of $2.74 billion. Revenue growth guidance is for around 30% for both Q1 and full year 2026, suggesting management sees momentum continuing beyond the strong Q4.

Yet the underlying set-up here is mixed, not euphoric, in spite of the overnight reaction. On one side, the beat and the raised full-year outlook fuel optimism, particularly around the company’s AI and edge computing story.

On the other, the stock’s premium valuation leaves Cloudflare a lot of work to do merely to justify its current $72.9 billion valuation. The rolling 12-month PE stands at an eye-popping 149.

Such multiples are not uncommon for high-growth stocks, but they do require plenty of confidence that the growth pace can continue. Cloudflare estimates its total addressable market to hit $196 billion by the end of 2026.

Looking at future growth

Perhaps the best way to access this with Cloudflare is to look at its new ACV bookings, or annual contract value. These smooth out contact timing to show the underlying annual value of a booking in the years to come. The cloud security and performance company continues to expand its market presence with ACV up nearly 50% year-on-year, a powerful signal of future revenue.

However, conversion timeline is critical. Management noted that about 20% of ACV in Q4 2025 was booked, the rest set to flow through 2026. This means a significant portion of that strong booking growth will flow through the income statement over the coming quarters, not immediately. The AI hype is driving this pipeline, but the market will need to see that pipeline convert into the promised revenue acceleration.

The growth trajectory is compelling, and the large customer momentum is real. But operating margins have come under a lot of pressure in recent years, perhaps a sign of intense competition and higher running costs.

Can it meet its 14% operating margin target in 2026 after guiding 11% for Q1 (14% in 2025). Time will tell but scaling a platform at this velocity comes with friction.

You might Also like: