")

Cybersecurity ‘darling’ CrowdStrike (CRWD) topped $5.25 billion in ARR (annual recurring revenue) in a record year. The Austin, Texas firm reported Q4 2026 results (to end Jan) that topped Wall Street estimates. Additionally, it issued largely in-line guidance for fiscal 2027. At a time when investors have been seriously spooked by talk of AI disruption across the software sector, the market’s response can be seen as a big positive.

Shares of the cybersecurity firm are up 0.7% in pre-market US trading Wednesday, holding $394 levels.

| CrowdStrike (CRWD) | Price: $394 (+0.66%) | Market cap: $99.33bn |

Of course, calling it a darling needs context after the stock’s sharp 17% sell-off since late January. November peaks of $557 seen like an age ago. The rise of advanced AI models capable of performing complex digital tasks has raised questions about the durability of growth among software-as-a-service (SaaS) companies.

Q4 and guidance

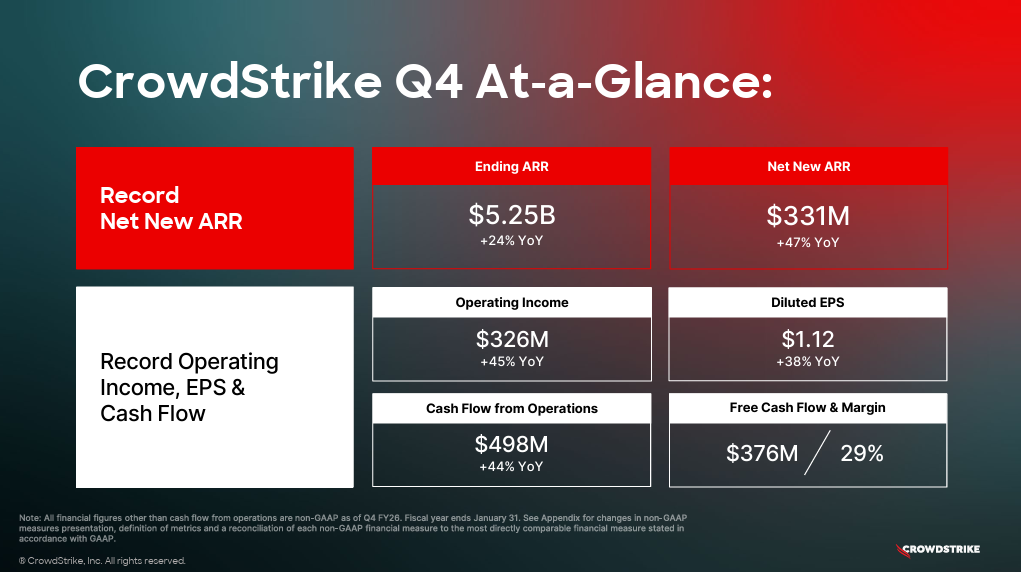

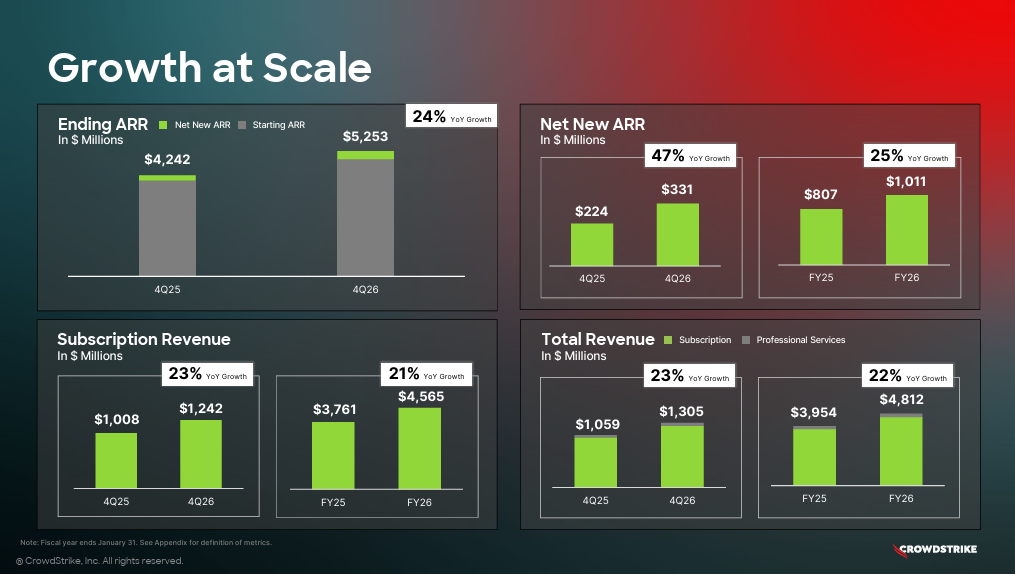

CrowdStrike posted Q4 earnings of $1.12 per share, beating analyst estimates of $1.10. Revenue rose to $1.31 billion, slightly ahead of the $1.30 billion consensus.

EPS is forecast to stand at $1.06-$1.07 for Q1 2027 versus $1.07 forecast, on $1.36 billion-$1.364 billion, versus the $1.36 billion consensus outlook.

For the full year, the company projected EPS $4.78-$4.90 against estimates of $4.84. This is on a $5.87 billion-$5.93 billion revenue range. That compares with consensus projections of $5.87 billion.

Of its $5.25 billion ARR, a fraction more than $1 billion was net new ARR. The company said it delivered record operating and free cash flow in both the quarter and the full year.

AI threat or opportunity

Interestingly, CrowdStrike mentioned AI 33 times on its earnings call. The firm focused on areas like securing enterprise AI deployments (from GPU to application layer). It also discussed monitoring AI applications running on endpoints. CrowdStrike said it now tracks 1,800+ AI applications and nearly 160 million instances across customer environments. Additionally, it discussed AI across its Falcon platform, and AI’s role in expanding the cybersecurity attack surface and demand for protection.

This is important given the recent (current) market mood on SaaS businesses. Investors are worried that AI could destabilise subscription streams down the line… the company, and most analysts, say the opposite.

Analysts have said those concerns may be overstated for cybersecurity providers, which remain core to enterprise IT spending.

‘Major growth driver’

CEO George Kurtz emphasised that the rise of enterprise AI is a major growth driver. He argued that organisations deploying AI systems need cybersecurity infrastructure to protect models, data pipelines, and endpoints.

Management said adoption of AI across enterprises is creating additional demand for security tools. This is positioning CrowdStrike to expand as companies secure AI workloads and data.

‘Overall we view this as a solid print, and continue to believe the company is a well-positioned cybersecurity platform consolidator and AI beneficiary given the unique data it creates, its best-in-class technology/broadening portfolio, and its ability to both secure AI and use AI to improve security’, analysts at Stifel said in a note.

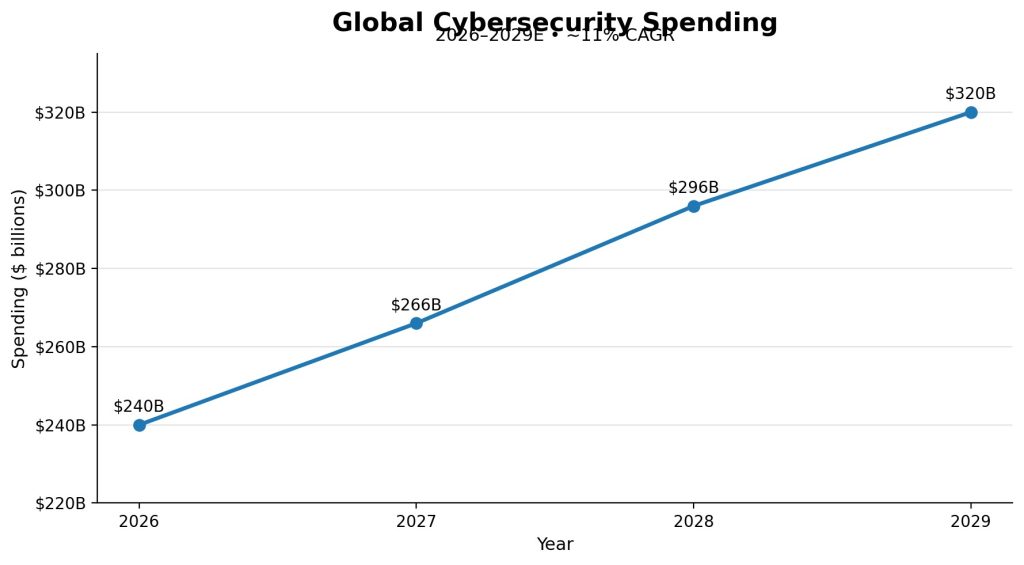

AI isn’t magic, but a complex web of programming protocols that need specific enterprise environments to work within. This suggests that AI expands the cybersecurity market, not shrinks it. JPMorgan estimates that AI-driven cybersecurity spending will grow at 3-4 times the rate the broader market suggests. The companies adapting to this new reality will benefit enormously.

The key is investing in companies that are leveraging AI to strengthen their offerings rather than being disrupted by it… as CrowdStrike is.

JPMorgan estimates AI cybersecurity growing 3x-4x faster

You might also like:

")