Cybersecurity bellwether Palo Alto Networks (PANW) continues to outperform quarterly expectations, but soft guidance was where investors concentrated. The market reaction suggests investors remain highly sensitive to profitability outlooks.

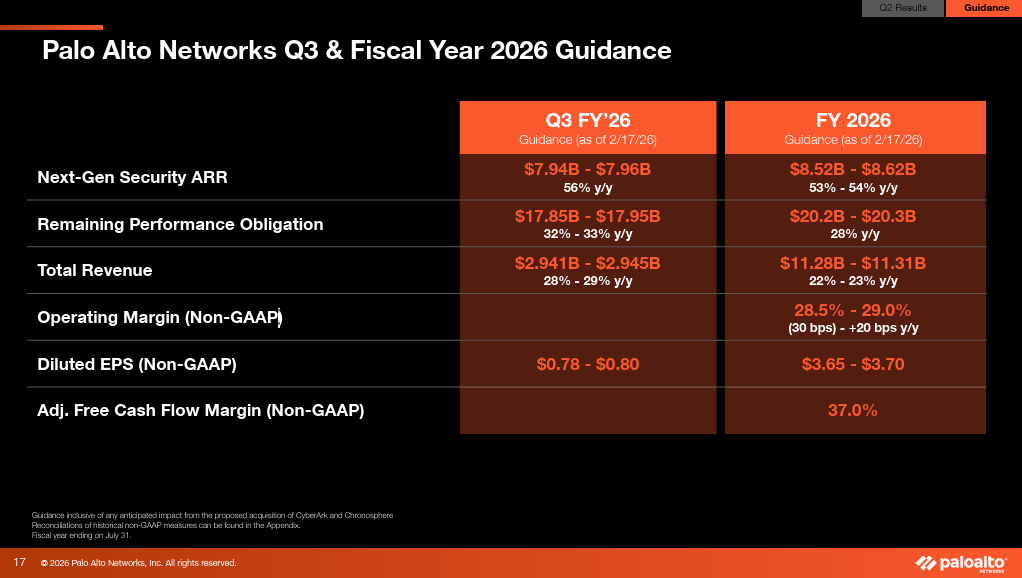

Palo Alto now expects fiscal 2026 (to end July) earnings per share of $3.65 to $3.70, down from its prior outlook of $3.80 to $3.90 and below the $3.87 consensus estimate. That the Santa Clara-based company upped revenue expectations were shrugged off by markets.

Palo Alto raised its full-year revenue forecast to a range of $11.28 billion-$11.31 billion, up from $10.50 billion-$10.54 billion previously and ahead of market expectations.

The stock is down more than 7% pre-market to a near two-year low.

| Palo Alto Networks (PANW) | Price: $151.85 (-7.22%) | Market cap: $122.9bn |

For the current quarter, Palo Alto projected EPS of $0.78 to $0.80 on revenue of $2.941 billion to $2.945 billion. Analysts had been looking for $0.92 on revenue of $2.61 billion, suggesting near-term margin pressure even as sales accelerate.

Solid Q2 overshadowed

Palo Alto, which provides AI-driven cybersecurity platforms spanning firewalls, threat intelligence, zero-trust architecture and secure access service edge (SASE) solutions, reported fiscal Q2 EPS of $1.03 on revenue of $2.59 billion. That topped analyst expectations of $0.94 EPS on $2.58 billion revenue.

Palo Alto counts nine of the 10 Fortune 10 companies among its customers, along with eight of the 10 largest US banks. Additionally, it counts six of the world’s 10 biggest oil and gas companies. This underscores its deep penetration in large enterprises.

Chief Executive Nikesh Arora said demand trends remain robust, highlighting accelerating ‘platformisation’ as customers consolidate vendors and modernise security stacks amid the rise of AI. He added that adoption of AI-focused security tools was steady and is expected to remain a long-term growth driver. In summary, Palo Alto outperforms quarterly expectations but soft guidance where investors concentrate shows the delicate balance between robust demand and cautious outlook.

Analysts at BofA Securities said they expect AI-related revenue to ‘inflect meaningfully’ over the next two years. Even in a scenario where AI significantly reshapes the security landscape, they argued that meaningful disruption to incumbent vendors remains unlikely in the near term. They also noted that large language models still lack the precision to replace core security controls.

The market reaction suggests investors remain highly sensitive to profitability outlooks, even as AI-driven demand continues to support top-line growth. Moreover, Palo Alto outperforms quarterly expectations but soft guidance where investors concentrate is likely to remain a theme. This continues as markets respond to each financial update.

Turning sentiment back in its favour is the challenge given limited evidence of the impact AI may extract on short-term performance. Furthermore, there is limited evidence for the longer-run story.

You might Also like: