AIM-listed infection prevention business Tristel (TSTL) is an attractive growth company with strong margins and a strong balance sheet. Given its potential to ‘clean up’ in the US market, where revenue is growing exponentially, it is also undervalued.

Tristel makes and distributes chlorine dioxide for the healthcare sector, where surfaces and medical devices need disinfecting to reduce risks to patients and staff.

Volume sales are growing at double digits, while the firm is also able to increase prices at or above inflation. The growth opportunity in the US, where sales rose sixfold in 1H26, means analysts and investors are under-pricing the shares.

| Share price: 393p | PE: 22.6x |

| Market cap: £188m | Yield: 3.6% |

What does the company do?

Tristel produces an HLD (high-level disinfectant) for medical devices, sold under the Tristel brand, and a sporicidal surface disinfectant sold under the Cache brand.

Tristel is used in medical settings including ENT (ear, nose and throat), cardiology, obstetrics and gynaecology, ophthalmology, optometry and urology. Alongside Tristel, the firm’s ‘3T’ digital compliance platform provides medical staff with full training, decontamination traceability and device management.

Cache is an economical, more sustainable alternative to low-level universal disinfectant wipes, cleaning while reducing hospital waste.

The firm is in the early stages of its push into the US healthcare market. This follows updated standards recognising chlorine dioxide foam as a recommended means of high-level disinfectant for medical devices.

We believe Tristel is on the verge of a new era of growth which the market has yet to recognise. We see the shares trading between 40% and 65% above today’s level in the next year and potentially significantly higher further out.

A large and growing opportunity

For the financial year to June 2025, the firm increased revenue by 11% to a record £46.5 million. It achieved this with a gross margin of 81%, meaning total selling costs were less than 20% of sales.

Adjusted EBITDA increased 20% from £10.8 million to £13 million, with a margin of 28% against 26% previously. Adjusted pre-tax profit rose 23% to £10.1 million, while adjusted EPS rose 12% from 15.3p to 17.15p.

The firm engaged with around 200 US health systems following the administration’s recommendation of chlorine dioxide as a high-level disinfectant. Meanwhile, a study with the Mayo Clinic concluded Tristel ULT was an effective and efficient disinfectant method for ultrasound probes.

With more devices being used for medical procedures, including ultrasound at the point of care, the market is growing. The danger of antimicrobial resistance, together with the need for compliance and traceability during disinfection, is also contributing to growth.

The firm believes the total addressable market for medical device disinfection is over £1 billion/year against £40 million of sales in FY25. The total market for surface disinfection is £5 billion against just £4 million of sales in FY25.

With US market expansion, new product launches, software commercialisation and inorganic opportunities, the firm sees sales growth accelerating. From a 10% compound annual rate between 2016 and 2025, sales are projected to rise by 17% annually into 2030.

Tristel financial performance 2015-2025

| FY15 | FY25 | Change | |

| Revenue | £15.4m | £46.5m | 202% |

| Operating profit | £2.5m | £8.4m | 236% |

| OPerating margin | 16.2% | 18.1% | +190bps |

| Cash from operations | £2.6m | £10.3m | 296% |

| EPS | 5.4p | 17.15p | 217% |

| DPS | 5.7p | 14.2p | 148% |

| ROCE | n/a | 22.1% |

Source: Tristel

Positive current trading, sales accelerating

For H1 to December 2025, sales increased by 14% to £25.65 million with 11% volume growth and 3% price hikes. That represents an acceleration from FY25’s 11% total sales growth rate.

UK revenue rose 13% while US revenue including direct sales and royalties increased six-fold helped by new product launches. Analysts are already racing to increase their forecasts for US sales in FY26 and FY27.

Gross margins were steady at 81% while adjusted EBITDA increased by 27% to £7.34 million representing a 28.5% margin. That isn’t just ahead of the firm’s current target, but also its medium-term 25% margin target.

Chief executive Matt Sassone said he was ‘particularly encouraged by progress in the United States’. Growth was driven by ‘accelerating ULT product sales, expanding clinical validation and favourable developments in US clinical guidance’, added Sassone.

Adoption by leading healthcare institutions and increasing utilisation metrics ‘reinforce our confidence in the scalability of the US ultrasound opportunity’, concluded the CEO.

Current forecasts

| FY26E | FY27E | |

| Revenue | £51.1m | £56.2m |

| Adjusted EBITDA | £14.3m | £15.6m |

| EBITDA Margin | 28% | 27.7% |

| Adjusted pre-tax profit | £1.2m | £12.4m |

| EPS | 17.7p | 19.4p |

| DPS | 14.6p | 15.1p |

Source: Cavendish Securities, data correct as of 2 March 2026

An attractive valuation

Turning to valuation, the shares currently trade around 390p which is where they were at the end of 2019. For comparison, earnings per share in FY20 were 12.35p against a consensus of 17.35p this year.

In other words, the shares trade on a forward PE of 22.6 times today against 31.8 times just over six years ago. Considering the potential upside from the US business, that looks completely wrong to us.

Leaving aside the fact that FY26 estimates are too low to start with, Tristel has compounded earnings by over 20%/year since 2005. Any firm which can achieve that level of growth ought to be trading at a premium rating.

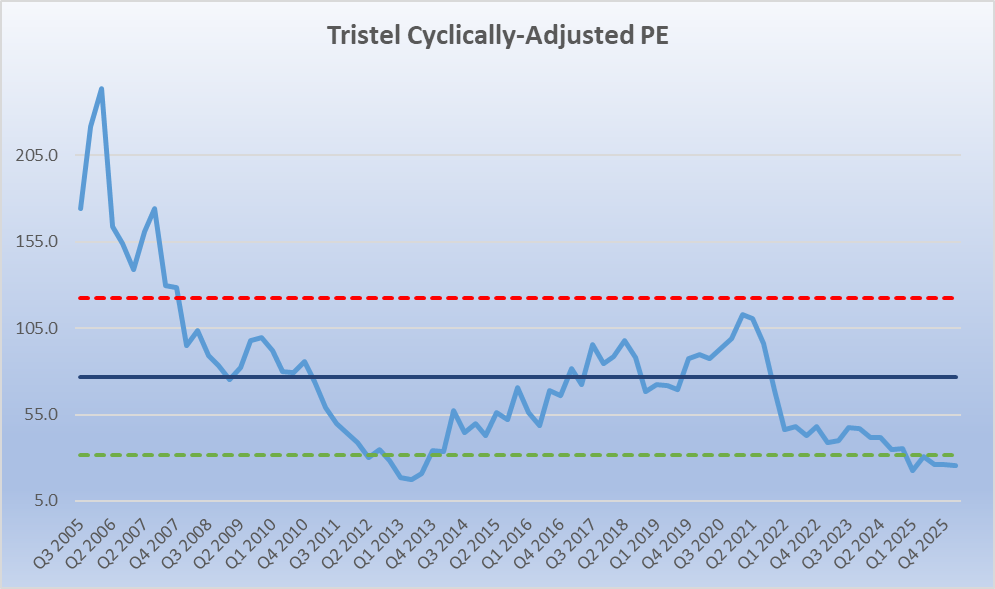

Yet, as the chart below shows, on a long term cyclically adjusted PE basis the shares are cheap relative to their history. Rather than a premium, they are trading more than one standard deviation below their 20-year mean.

Being conservative, if the shares returned to -1 SD (the green line) in six months, they would trade at 543p. If they took another year to reach -1 SD, they would be trading at 650p, level with their 2021 highs. If they actually reverted to the mean (blue line), however, we would be talking several multiples of the current share price.