Investors in Smiths (SMIN) are being asked some tough questions as the FTSE 100 multi-national engineering business reshapes its business. Today’s announcement confirmed sweeping changes that will see parts of the business sold. In addition, there will be a fresh £1.5 billion capital return to shareholders. This comes alongside seemingly solid half year trading.

That all sounds positive, so why have the shares plunged, down more than 8% in morning trading?

| Smiths (SMIN) | Price: £21.52 (-8.4%) | Market cap: £6.71bn |

Profit growth amid portfolio overhaul

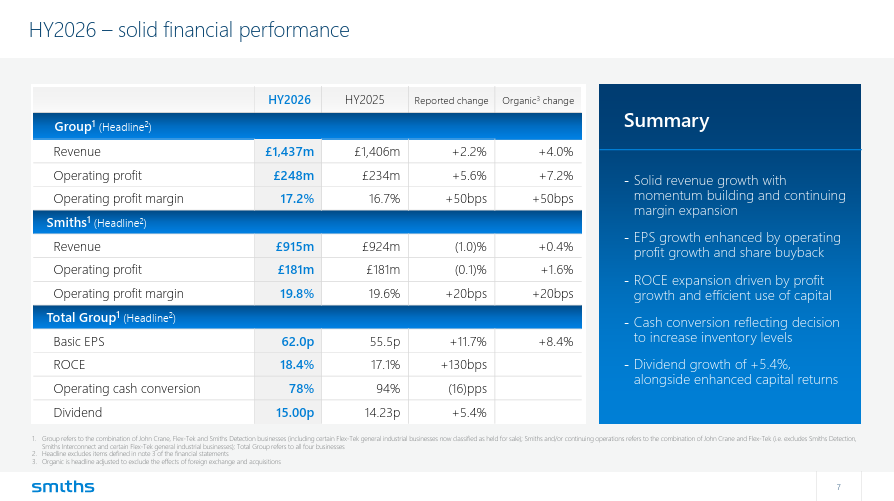

For the six months ended 31 January, Smiths posted a 5.6% rise in headline operating profit to £248 million, supported by a 2.2% increase in revenue to £1,437 million. But it can be argued that short-term trading performance is not the real story here. Instead, the company pushes ahead with its operational overhaul.

Smiths is smack bang in the middle of stripping back its operations to concentrate on parts of the business where growth opportunities are best and margins higher. Chief executive Roland Carter described the half as ‘transformational’. He referenced the disposals of its Detection and Interconnect divisions, both sold at earnings multiples materially above market expectations.

Smiths Detection is being sold to CVC Capital Partners for an enterprise value of £2.0 billion. This is a valuation equivalent to 16.3x FY2025 headline operating profit, consistent with terms announced in December 2025. The deal is expected to close in the second half of 2026. However, this is subject to regulatory approvals.

Meanwhile, the £1.3 billion sale of Smiths Interconnect to Molex advances the company’s strategic repositioning. Now the focus is around its two core divisions, John Crane and Flex‑Tek.

Organic growth pace

The trouble is, at the moment, those remaining business units are patchy. Organic growth came in at 0.4% on rough 20% margins. Investors will need to see better organic growth than this going forward.

At least management are confident the firm is heading that way. Smiths reaffirmed its full‑year outlook, anticipating 3%–4% organic revenue growth for continuing operations. H2 performance is expected to fall within its medium‑term guidance range of 5%–7% organic growth, with operating margins around 20%.

Importantly, potential disruptions from the Iran conflict have not yet been fully factored into guidance, so that’s something to follow.

In the meantime, following a £500 million share buyback completed in December and another £1 billion programme currently underway, Smiths plans to return an extra £1.5 billion to investors. The mechanism will include a structured return – either via a tender offer or special dividend. In addition, there will be a further buyback once the Detection sale has completed later this year.

There are lots of moving parts to the Smiths investment story right now, which possibly explains the market’s reaction today. That said, there’s a clear operational plan and the promise of boosted shareholder returns to come.

But swirling uncertainly in the Middle East clearly isn’t helping. That probably explains the stock’s 20%+ share price drop since late February. By contrast, there was a 60%-odd rally in the 10 months up until then. The 12-month rolling PE of 18.5 leaves plenty of downside risk if execution isn’t spot on.

You might also like: