Investors expected a lot from memory chip manufacturer Micron Technology (MU). They got plenty, but not enough it seems. Pre-market data has the stock down nearly 7%, so what’s caused the kerfuffle?

The short answer is cash, spending it, lots of it. Micron unveiled plans to invest more than $25 billion in new manufacturing capacity in fiscal 2026 (to end Aug), about $5 billion more than expected, or roughly 60% of last year’s net profit.

If there’s one thing we’ve learned in 2026, it’s that markets now want a much clearer link between investment and returns, especially when it comes to AI capex.

Investing to grow

Still, the reaction looks odd. Micron is one of the world’s few expert manufacturers of both DRAM and NAND memory chips, and the sole US-based. That puts it right at the centre of one of AI’s biggest bottlenecks.

‘In the AI era, memory has become a strategic asset for our customers, and we are investing in our global manufacturing footprint to support their growing demand’, said Micron CEO Sanjay Mehrotra.

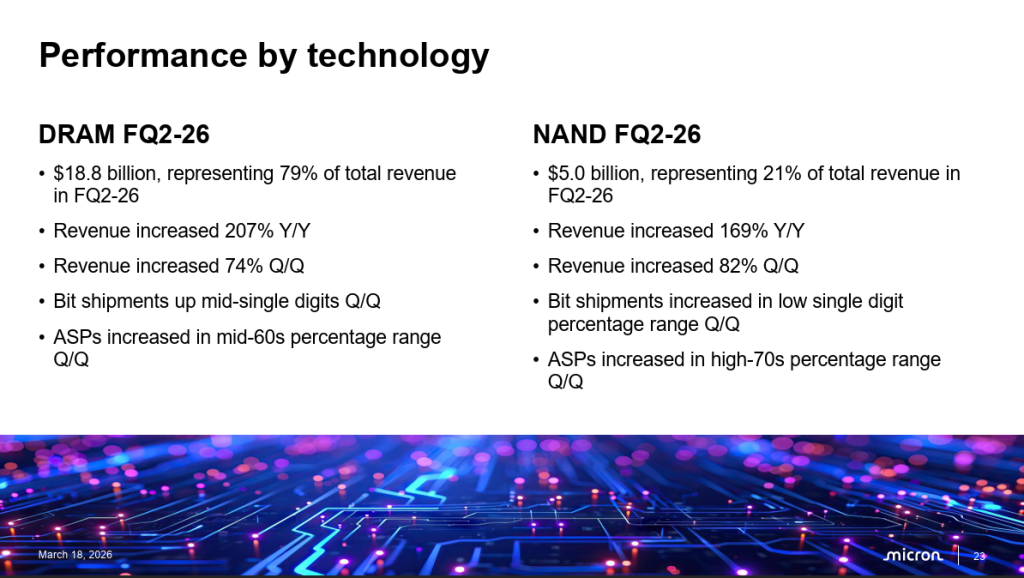

DRAM, which accounted for 79% of total revenue, brought in $18.77 billion, up 207% year-on-year. NAND revenue rose 169% to $5 billion.

The explosion of AI datacentre build-outs has resulted in demand that far outweighs supply, with Mehrotra stating that tight conditions for DRAM and NAND are expected to persist ‘through and beyond’ 2026.

You don’t need to be an economist to know that when demand outstrips supply, prices go up, and up they are zooming up for Micron – in the mid-60% for DRAM, high-70% for NAND, something we flagged on our recent podcast (tune in here).

Little wonder that fiscal Q2 revenue nearly tripled year-on-year and EPS jumped nearly 8-fold. Sure, the stock has rallied hard in 2026, up 46%, but the PE at 9 (on a 12-month rolling basis) is no higher than long-run averages of 6-20 ish.

Record margins

The Idaho-based company posted adjusted EPS of $12.20 for the quarter, against $1.56 a year earlier and above analyst consensus of $8.79. Revenue rose 196% to $23.86 billion from $8.05 billion a year ago, beating estimates of $19.19 billion.

Gross margin hit 74.9%, up 18 percentage points sequentially and a company record.

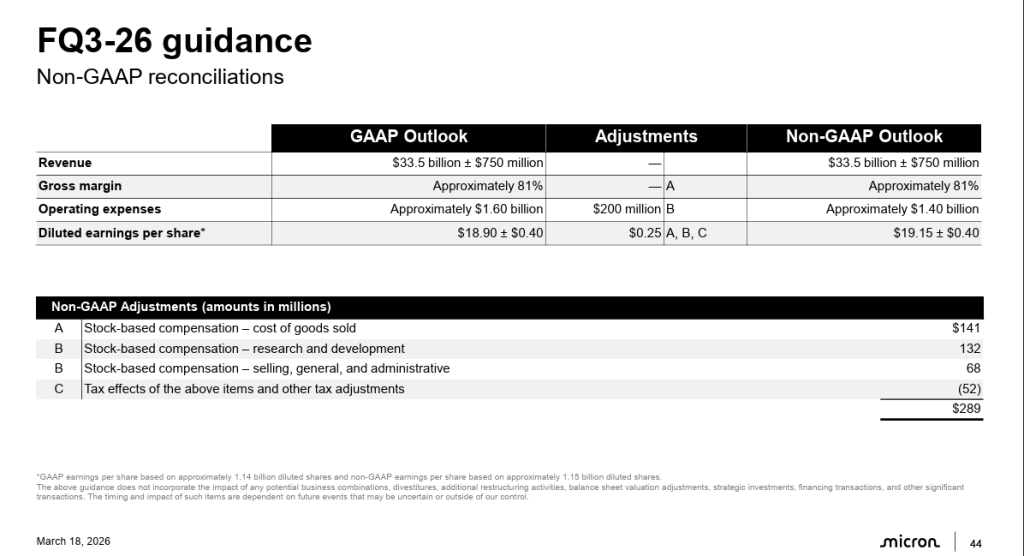

For the current quarter ending May, Micron guided revenue of $33.5 billion, plus or minus $750 million, against analyst estimates of $24.29 billion. Adjusted EPS guidance of $19.15 was nearly double consensus of $12.03. Gross margin is forecast at 81%, up 610 basis points sequentially.

Raymond James raised its price target to $530 from $310, citing record revenue across all business units, record margins and record free cash flow, noting that with gross margin guided to 81% in the third quarter, incremental price increases would have a diminished impact on further margin expansion.

Morgan Stanley raised its price target to $520 from $450, maintaining an ‘overweight’ rating, and said it expects adjusted EPS of at least $80 to be sustainable through calendar 2027.

Analysts said the post-earnings share decline, after a roughly 100% gain since the prior quarter, reflects low conviction on the durability of results rather than near-term fundamentals. Perhaps the market is right to be wary – the chip industry is notoriously cyclical.

Yet the risk/reward balance looks firmly tiled towards the latter right now, and the market is wrong to punish long-term investment in the business.

You might also like: