")

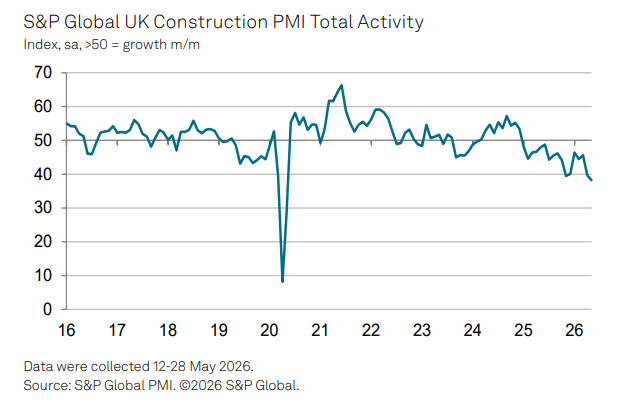

UK construction activity in May showed its sharpest decline in six years as measured by the S&P Global UK Construction PMI. Excluding the pandemic, the fall was the worst since March 2009 during the global financial crisis.

The UK Construction PMI (Purchasing Managers’ Index) dropped from 39.7 in April to 38.2 last month, the steepest fall since May 2020. The figure also extended the run of sub-50 readings, which signals a contraction in activity, to 17 consecutive months.

S&P attributed the decline to shrinking order books and rising economic uncertainty. At the same time, higher energy, fuel and transport costs led to the fastest rise in input price inflation since June 2022.

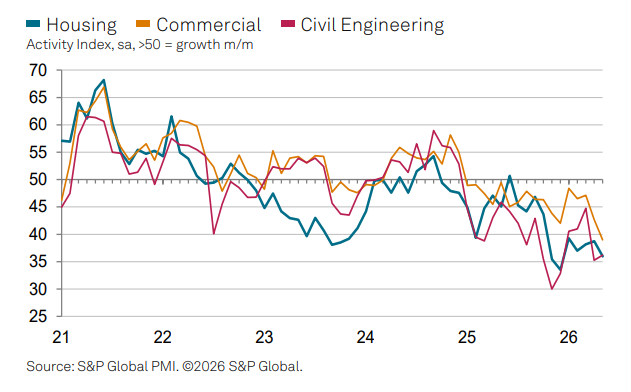

All three broad categories of construction – residential, commercial and civil engineering – posted a sharp decline. Residential activity was the weakest area, with managers citing ‘unfavourable market conditions and headwinds from elevated borrowing costs’.

Commercial construction activity fell as clients became more risk averse in response to geopolitical tensions and rising costs, said S&P. Civil engineering activity fell but at a slower pavce than in April.

Companies said project delays, deferred investment decisions and general cutbacks to clients’ budgets had all resulted in fewer tender opportunities. Some suggested domestic political uncertainty had also impacted demand conditions in May.

Worryingly for building materials firms, the lack of new orders and tenders meant another sharp drop in buying. The fall in purchasing activity in May was the fastest in over six months.

The only bright spot was in infrastructure with firms looking forward to forthcoming energy sector and power network projects.

We have recommended avoiding housebuilders for a long time and now unfortuantely the data supports our call. Residential construction activity is the weakest part of the market and may make a new low for this cycle.

Commercial activity is already hitting a cycle low, just not as low as housebuilding, while civil engineering has stabilised, sort of. However, it’s not just the slowdown in activity which is spooking purchasing managers.

Input prices are rising fast, and just as concerning, suppliers’ delivery times have slipped for the third month running. There are widespread reports of international shipping delays and some raw material shortages are starting to creep in.

None of this is good for the construction industry, and although we still like infrastructure companies few are cheap any more. Stocks like Balfour Beatty (LON:BBY), Keller (LON:KLR) and Morgan Sindall (LON:MGNS) have mean-reverted, while Galliford Try (LON:GFRD) looks increasingly overvalued.

INVESTOR EVENTS

Join our inaugural Investor Webinar on at 6pm Wednesday 24 June for a look inside the world of investment trusts. Hear directly from managers as they discuss how they are navigating today’s markets, where they are finding opportunities, and how portfolios are being positioned for the months ahead.

This is a chance to go beyond the headlines and understand the real decisions being made inside trust portfolios. A live Q&A will follow, giving investors direct access to the managers and the opportunity to ask questions on performance, strategy, and outlook.

Click on the link below to register for this free event:

")