Trustpilot (LON:TRST) delivered another strong trading update on Thursday, 16 July, with growth ahead of analyst expectations and management highlighting artificial intelligence as an increasingly powerful demand driver. Enterprise customer wins, particularly in North America, continue to accelerate and management reiterated full-year guidance, reinforcing confidence that the business remains one of the UK’s more attractive structural growth stories.

For UK retail investors, the key question is no longer whether Trustpilot is growing—it clearly is—but whether today’s valuation already reflects much of that optimism.

| Trustpilot (LON:TRST) | Price: 261.60p (-10%) | Market cap: £1.01bn |

What does Trustpilot do?

Trustpilot operates one of the world’s largest online consumer review platforms, helping businesses collect, manage and showcase customer reviews while enabling consumers to make informed purchasing decisions.

Its subscription-based software helps businesses:

- Collect verified customer reviews

- Improve online reputation

- Generate marketing content

- Analyse customer feedback

- Improve visibility across Google and increasingly AI-powered search engines

Management increasingly believes AI is becoming a major competitive advantage because large language models increasingly cite trusted review data when answering consumer questions.

H1 2026: Reported vs expectations

| Metric | Reported | Market expectation | Verdict |

| Bookings | $171m | ~$171m | In line |

| Revenue | $151m | Slightly below reported | Beat |

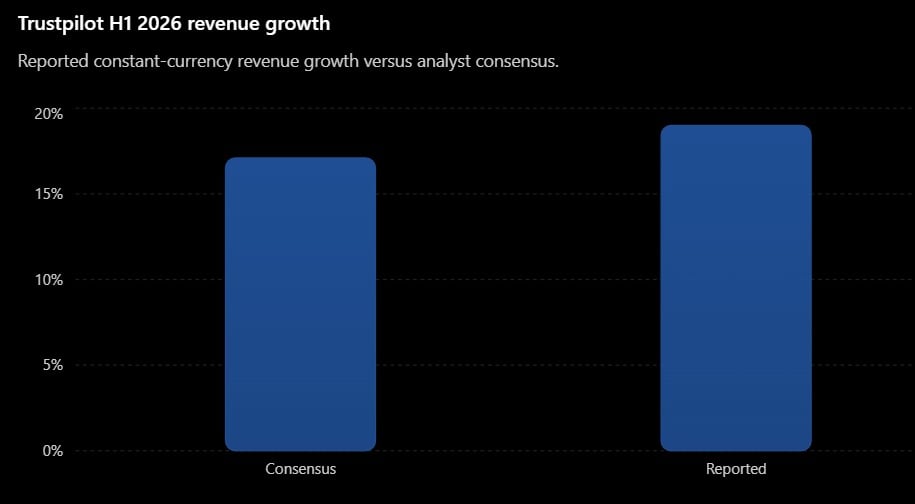

| Revenue growth (constant currency) | 19% | 17.1% | Beat |

| ARR | $313m | Above $300m expected | Beat |

| Gross retention | 87% | Stable | Positive |

| Net cash | $21.9m | Lower after buybacks | Expected |

| FY26 guidance | Reiterated | High-teens growth | Positive |

Source: Company trading update and analyst consensus.

Market reaction

Investors welcomed another quarter of accelerating enterprise demand and improving profitability, but evidently were left flat after management failed to push guidance even higher. Today’s 10% share price fall may look harsh, but investors must consider this reaction in context – the stock had rallied ~85% YTD ahead of today’s results, and it remains 66% up today.

Trustpilot emerges as clear AI winner as profit and traffic surge

The biggest positives were:

- Revenue growth exceeded analyst expectations.

- North America remained the fastest-growing region.

- Enterprise customers continue to spend more.

- AI is becoming an additional growth catalyst rather than a threat.

- Management reiterated full-year guidance.

Those factors reinforced confidence after a very strong FY2025 performance and suggested the company’s operational momentum has continued into 2026.

What management said

CEO Adrian Blair struck an optimistic tone, saying:

‘AI is proving a significant tailwind for customer growth… businesses increasingly understand the value of Trustpilot feedback in the age of AI.’

Management highlighted several important trends:

- Enterprise annual recurring revenue grew strongly.

- Customers spending more than US$20,000 annually increased rapidly.

- ChatGPT-related requests increased more than 400% year-on-year.

- Trustpilot believes it is becoming an important ‘trust signal’ within AI-powered search results.

- Shopify integration continues to strengthen the ecosystem.

Why AI could be a game changer

Historically Trustpilot benefited from Google search traffic.

Now management believes the next growth engine could be AI search.

If consumers increasingly ask ChatGPT or other AI assistants which retailer, airline or bank they should use, trusted review datasets become much more valuable.

Rather than replacing Trustpilot, AI could increase demand for its data and encourage businesses to subscribe to improve their visibility in AI-generated answers.

Opportunities

| Opportunity | Why it matters |

| AI search | New demand for trusted review data |

| Enterprise expansion | Larger customers deliver higher margins |

| North America | Largest long-term growth market |

| Margin expansion | Significant operating leverage remains |

| Buybacks | Support EPS growth and shareholder returns |

Risks

| Risk | Why investors should watch |

| Premium valuation | Leaves little room for disappointment |

| Slower SME demand | Smaller businesses remain economically sensitive |

| Competition | Google Reviews and other review platforms remain strong competitors |

| AI platform dependence | Search behaviour could evolve unpredictably |

| Retention | Net retention remains only just above 100% |

What analysts are watching

Analysts remain constructive because Trustpilot continues to execute ahead of expectations.

The biggest themes include:

- Can revenue growth remain in the high-teens beyond 2026?

- Will AI continue driving enterprise adoption?

- How quickly can EBITDA margins move towards management’s medium-term targets?

- Can North America become the group’s largest profit contributor?

Consensus prior to the update anticipated around 17.1% constant-currency revenue growth and an adjusted EBITDA margin of roughly 18%, so today’s trading update modestly exceeded expectations while leaving guidance unchanged.

Investor verdict

Trustpilot increasingly looks like one of the UK’s highest-quality software growth businesses, with artificial intelligence an increasingly powerful demand driver. Revenue continues to compound at close to 20%, profitability is improving, cash generation remains healthy and management has successfully positioned the platform to benefit from AI rather than be disrupted by it.

The investment case now depends less on whether the business can grow and more on whether it can sustain premium growth for several years. With enterprise adoption accelerating and AI creating new monetisation opportunities, the long-term outlook remains attractive. However, after a strong run in the shares, expectations are also much higher, meaning future updates will need to keep delivering consistent beats rather than simply meeting guidance.

Disclaimer: The author Steven Frazer has a personal interest in Trustpilot.

You might also like: