Shares in Snowflake (NYSE:SNOW) surged in extended trading after the company delivered a major Q1 FY2027 earnings beat and raised full-year guidance, reinforcing investor confidence that the company is emerging as one of the biggest enterprise AI infrastructure winners. Pre-market gains are running at +37%, which would add roughly $22.5 billion to the market cap, one of the stock’s strongest post-earnings reactions since its IPO.

| Snowflake (NYSE:SNOW) | Price: $242.40 (+37%) | Market cap: ~$83bn |

For UK retail investors, the key takeaway is that Snowflake is no longer being valued purely as a cloud data warehouse provider. The market increasingly sees it as a critical ‘AI data layer’ that helps enterprises organise, govern and deploy AI workloads securely across massive datasets.

📊 Q1 FY2027 key numbers

| Metric | Reported | Wall Street Expectation | YoY Growth |

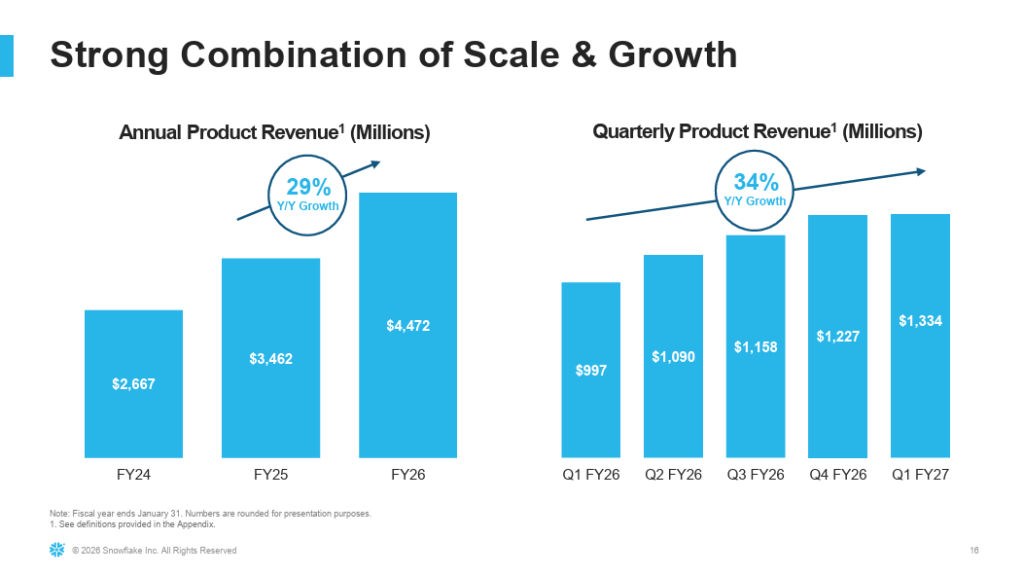

| Revenue | $1.39bn | $1.32bn | 34% |

| Product Revenue | $1.33bn | ~$1.30bn | 34% |

| Adjusted EPS | $0.39 | $0.32 | 22% beat |

| Net Revenue Retention | 126% | ~125% expected | Improving |

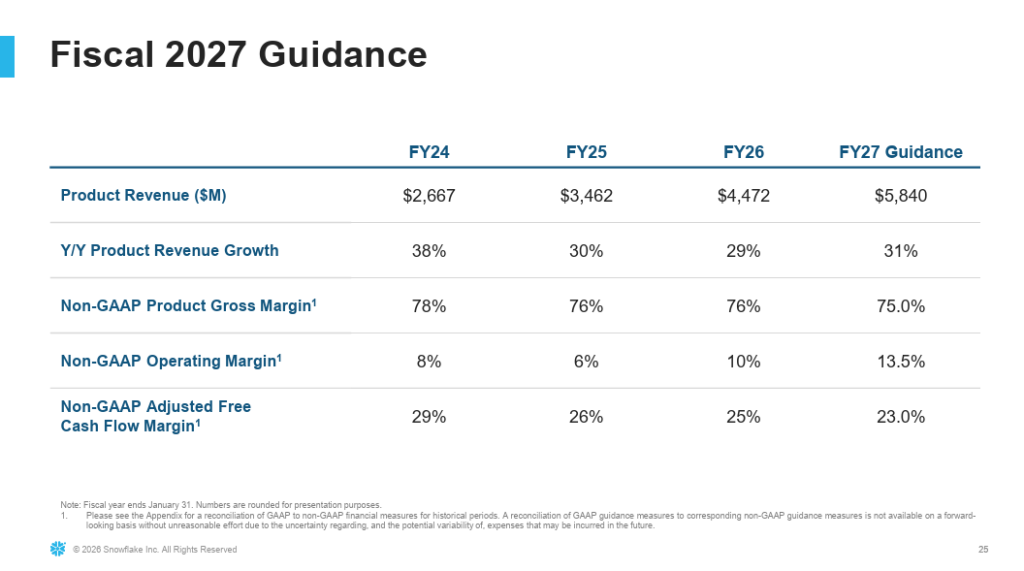

| FY2027 Product Revenue Guide | $5.84bn | Prior $5.66bn | 31% growth |

📈 Why the stock exploded higher

The biggest surprise was not simply the earnings beat, but evidence that AI demand is accelerating customer spending again after concerns earlier in 2026 that growth was slowing.

Management highlighted:

- accelerating adoption of Snowflake Intelligence and Cortex AI tools

- strong growth in large enterprise customers

- improving net revenue retention

- rising AI-related consumption workloads

- a huge new $6 billion multi-year strategic partnership with Amazon Web Services

That AWS agreement matters because it effectively ties Snowflake deeper into enterprise AI deployment infrastructure over the next five years.

CEO Sridhar Ramaswamy described the quarter as a ‘milestone’ for the company’s AI transition, while analysts increasingly refer to Snowflake as a potential ‘control plane’ for enterprise AI applications.

💡 The AI opportunity

Snowflake’s investment case increasingly revolves around a simple idea: AI systems become vastly more valuable when connected to high-quality enterprise data.

That plays directly into Snowflake’s strengths:

- Enterprise data storage

- Governance and security

- AI model integration

- Real-time analytics

- Scalable compute consumption

The company said more than 7,100 accounts are already using Cortex Code tools, while adoption of Snowflake Intelligence more than doubled quarter-over-quarter.

Unlike some AI software names that remain highly speculative, Snowflake is already monetising AI through higher data consumption. That makes the growth more tangible for investors.

AI investing: Bubble or start of new economic supercycle?

🧠 Valuation: still expensive, but improving

Despite the rally, valuation remains the biggest debate surrounding Snowflake stock.

| Valuation Metric | Approximate Level |

| Market Capitalisation | ~$60bn |

| Forward Sales Multiple | ~18x–20x |

| GAAP Profitability | Still negative |

| FY2027 Revenue Growth | ~31% |

For comparison, traditional software firms often trade nearer 5x–10x forward sales. Snowflake therefore still commands a premium valuation because investors believe it sits near the centre of long-term AI infrastructure spending.

The bullish case is:

- AI demand could reaccelerate revenue growth above 30%

- margins are improving

- customer spending trends are strengthening

- Snowflake could become core AI infrastructure for large enterprises

The bearish case is:

- the valuation already prices in years of strong execution

- competition from hyperscalers and AI-native rivals remains intense

- the company still lacks consistent GAAP profitability

👉 What UK investors should watch next

For ISA and SIPP investors, Snowflake now looks more like a high-growth AI infrastructure stock than a traditional software company.

The next major indicators to monitor are:

- whether AI products become a material standalone revenue driver

- if net revenue retention continues improving above 125%

- sustained operating margin expansion

- whether enterprise AI spending remains resilient through 2026

If management can maintain 30%+ growth while improving profitability, many investors will argue today’s valuation is justified. But after such a dramatic after-hours move, volatility is also likely to remain extremely high.

You might also like: