Softcat (SCT) shares surged after the FTSE 250 IT infrastructure reseller delivered a stronger‑than‑expected first‑half performance. It also upgraded its full‑year profit outlook. Investors were looking for signals of resilient demand trends amid intensifying corporate investment in AI‑related technologies, and they got it in spades.

The £2.45 billion company now expects high single‑digit growth in underlying operating profit for FY2026 (to end July), up from a previous low single‑digit forecast. That raise follows a substantial earnings beat in the six months to January.

| Softcat (SCT) | Price: £12.43 (+8.1%) | Market cap: £2.45bn |

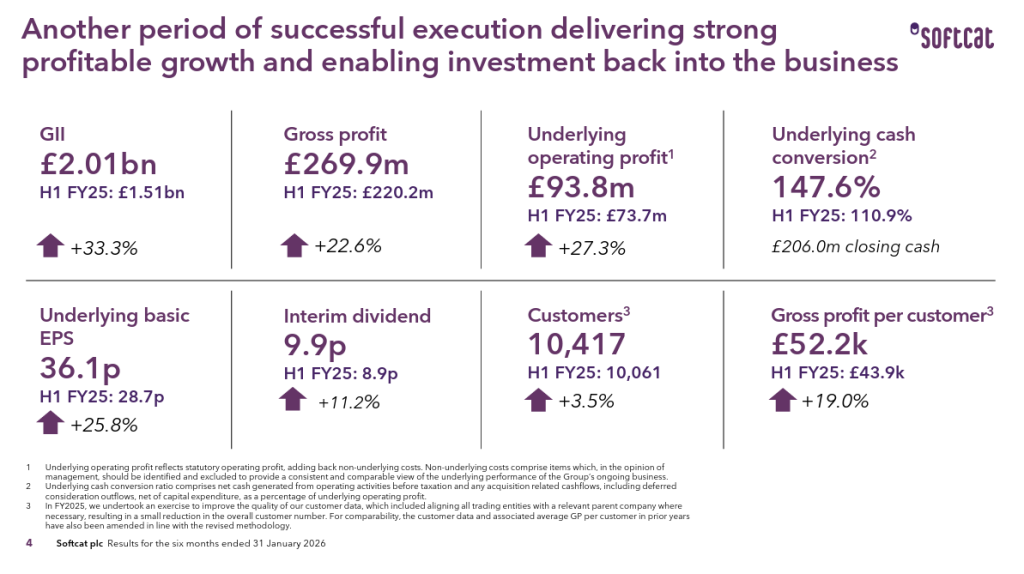

Underlying operating profit jumped 27.3% to £93.8 million, exceeding analyst expectations by roughly £12 million. Meanwhile, gross profit advanced 22.6% to £269.9 million, a figure that also came in about £18 million ahead of consensus. Crucially, the gross profit beat flowed almost entirely to operating profit. This underscored tight cost control and improved operational leverage.

Hardware drives growth

Top‑line momentum was equally strong. Gross invoiced income rose 33.3% to £2.01 billion, driven by a dramatic 79.1% surge in hardware billings. Hardware is currently the fastest‑growing segment. Management attributed this to strong datacentre, networking and compute demand. Much of it was tied to larger project wins and expanded AI‑focused infrastructure deployments.

Cash generation was another highlight with a headline cash conversion ratio of 147.6%, although this was inflated by a one‑off £42.4 million advance payment from a single customer. Even so, the underlying conversion rate stood at 102.4%, still comfortably above Softcat’s 85%–95% target range. Period‑end cash was £206 million, after £73 million in dividends and £22.4 million of the company’s £45 million buyback scheme. The interim dividend was raised 11.2% to 9.9p per share.

Pulled forward orders

However, a material portion of the earnings beat reflects timing factors rather than pure underlying acceleration. Softcat began the year with £290.3 million in unrecognised IFRS 15 contract liabilities. Around £140 million flowed into the first half, with the remainder due early in the second half. Management also noted that some customers pulled orders forward ahead of expected memory price increases. Sharesify has highlighted this before, though the scale of this effect was not disclosed.

Customer metrics strengthened, with the client base growing 3.5% to 10,400 and gross profit per customer rising 19%.

Softcat stock 1-year

Source: Softcat

Chief executive Graham Charlton said demand conditions remain favourable as organisations accelerate AI‑enabled infrastructure rollouts. He described the industry as being in only the ‘early stages’ of adoption.

Jefferies welcomed the beat but warned that FY2027 estimates are unlikely to rise proportionally. This is due to order timing and pull‑forward effects.

This was another robust half from Softcat and one that broadly reinforces the direction of travel seen last year. The demand backdrop remains supportive, particularly across datacentre and networking. Here, AI-driven infrastructure spend is clearly coming through, and Softcat continues to convert it well.

The upgrade to guidance is encouraging and it’s worth noting Softcat’s track record of pumping guidance up as it goes. This feels like more of the same.

Crucially, time will tell how much pulled forward demand impacts H2 and beyond. It remains to be seen how likely the stock is to return to 52-week peaks close to £19. But overall, underlying momentum looks solid.

You might also like: